The setting is familiar. It’s a cousin’s wedding, a Diwali card party, or a quiet Sunday lunch. You are enjoying your paneer tikka when Sharma Uncle—a distant relative, a retired neighbour, or perhaps your own Chacha ji—corners you.

After five minutes of polite small talk about your job and marriage prospects, the pivot happens.

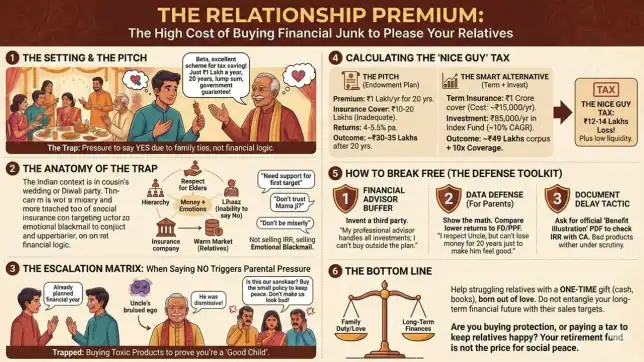

Beta, what are you doing for tax savings this year? I have an excellent scheme. Just ₹1 Lakh a year, and after 20 years, you get a lump sum. Full safety, government guarantee!

Your stomach tightens. You know a little bit about finance. You know that traditional endowment plans usually offer terrible returns (barely beating inflation) and ULIPs with high charges and inadequate insurance cover. You know you should buy a pure Term Plan and invest the rest elsewhere.

But looking into Sharma Uncle’s hopeful eyes, knowing that this agency is his post-retirement hustle or a way to fund his daughter’s education, your financial logic collapses.

🔥Secure your future with our Robo-advisory tool trusted by over 3,000 investors and advisors. From effortless retirement planning to funding your children’s biggest dreams, turn your financial goals into reality. 🔥

Subscribe for money management solutions via email! (Link takes you to our email sign-up form) Join 32,000+ readers in our community.

👉 New Tool Alert! NaviPlan: A Privacy-Focused Multi-asset Tracker and Goal Planner 👈

You say yes. You sign the cheque.

You didn’t just buy an insurance policy. You paid the Relationship Premium.

About the author: Ajay Pruthi is a fee-only SEBI-registered investment advisor. He can be contacted via his website plnr.in.

The Anatomy of the Trap

In India, money and emotions are impossibly tangled. We don’t just transact; we relate. Our social fabric is built on hierarchy, respect for elders, and a deep-seated inability to say no without offending.

Insurance companies know this. It is why the individual agency model thrives here. They aren’t recruiting financial experts; they are recruiting people with warm markets—a ready database of nephews, nieces, and neighbours who will find it socially awkward to refuse them.

When a relative pitches you a bad product, they aren’t selling Internal Rate of Return (IRR). They are selling emotional blackmail.

- I just started this agency; I need your support for my first target.

- Don’t you trust your own Mama ji with your money?

- This is for your future children, don’t be miserly.

The pressure isn’t financial; it’s social. You buy the product to avoid being the topic of gossip at the next family gathering as the arrogant youngster who thinks they know more than their elders.

The Escalation Matrix: When Saying No Triggers Parental Pressure

Sometimes, you summon the courage to set a boundary right there at the party.

You politely decline: Uncle, thank you for thinking of me, but I’ve already completed my financial planning for the year. I don’t have any investible surplus right now.

You feel proud of yourself for handling it maturely. You think the matter is closed.

It isn’t. You just triggered the escalation matrix.

Sharma Uncle’s ego is bruised. He sees your refusal not as a financial decision, but as disrespect from a junior who thinks they are too smart now that they earn a salary. He doesn’t argue with you; he goes straight to headquarters—your parents.

The next day, your father calls, and his tone is icy.

Beta, Sharma Uncle called me today. He was very upset. He said you were dismissive and rude when he was just trying to help you with your future. Is this what we taught you? To insult elders?

Suddenly, the narrative has shifted. It is no longer about a bad insurance product with 4-5% returns. It is now about Sanskar (values), disrespect, and the family’s reputation.

Your parents apply the ultimate guilt squeeze: Look, just buy the small policy to keep the peace. It’s only ₹50,000 a year. Don’t make us look bad in front of the relatives. We have to live in this society.

Now you are trapped. You buy the toxic product not because you want it, but to prove you are still a good child.

Calculating the Nice Guy Tax

The tragedy of the Relationship Premium is that while the emotional relief is instant (Uncle is happy, Dad is pacified), the financial pain lasts for decades.

Let’s look at the literal cost of being nice.

The Pitch: Uncle sells you a traditional Endowment Plan.

- Premium: ₹1 Lakh per year for 20 years.

- Insurance Cover: ₹10-20 Lakhs (woefully inadequate).

- The Reality: These plans typically generate returns of 4% to 5.5%. After 20 years, you might get back around ₹30-35 Lakhs.

The Smart Alternative: You politely decline and do it yourself.

- Term Insurance: You buy a pure term plan for ₹1 Crore cover. Cost: Approx ₹15,000/year.

- Investment: You invest the remaining ₹85,000 into a simple Index Mutual Fund (assuming a conservative 10% CAGR after tax).

- The Result: After 20 years, your mutual fund corpus is approx. ₹49 Lakhs (after tax), AND you enjoyed 10x-5x the insurance coverage the whole time.

The Cost of Niceness: You just paid a ₹12-14 Lakh tax just to avoid some awkward conversations. Furthermore, if you stop paying after 3 years, you lose a huge chunk of your principal.

How to Break Free (The Defence Toolkit)

You need a toxicity shield—a polite but firm set of scripts to decline these offers. When parents get involved due to the escalation matrix, you need stronger defences.

- The Financial Advisor Buffer (The Ultimate Shield)

Invent a third party if you don’t have one. This removes you from the equation.

- To Uncle: Mama ji, sounds good, but my professional financial advisor handles all my investments now. We have a strict plan, and I am not allowed to buy anything outside of it.

- To Parents: Dad, I can’t. My advisor showed me that if I lock money into this, I won’t be able to afford the down payment for a house next year. It ruins my cash flow plan. (Raise the stakes so they see the real cost).

- The Data Défense (For Parents)

Parents often push these products out of ignorance, not malice. They genuinely think it’s safe and that the uncle means well. Show them the math.

- Action: Sit down with your father. Pull up a calculator. Show him that the returns are lower than a Bank FD or PPF, which are safer. Say, Dad, why should I earn 4-5% here when the bank gives 7%? I respect Sharma uncle, but I can’t lose money for 20 years just to make him feel good. That’s not respectful to the hard work I do to earn it.

- The Document Delay Tactic

Bad products wither under scrutiny. Agents hate educated customers who ask for details.

- Script: Uncle, send me the official ‘Benefit Illustration’ PDF. I need to run it through Excel to check the IRR and show it to my CA before committing.

- The Result: 80% of the time, they won’t send it because they know the numbers look bad on paper.

The Bottom Line

It is noble to want to help your relatives. If your uncle is struggling, gift him cash on Diwali. Help pay for his child’s books. That is a one-time cost born out of love.

But do not entangle your long-term financial future with their sales targets.

Ask yourself: Are you buying an insurance policy for your family’s protection, or are you paying a tax to keep your relatives from getting upset? Your retirement fund should not be the price you pay for social peace.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

🔥You can also avail massive discounts on our courses and the freefincal investor circle! 🔥& join our community of 8000+ users!

Track your mutual funds and stock investments with this Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds, and ETF screeners, as well as momentum and low-volatility stock screeners.

You can follow our articles on Google News

We have over 1,000 videos on YouTube!

Join our WhatsApp Channel

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalised investment advice. We can write a detailed article without mentioning your name if you have a generic question.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

About The Author

Dr M. Pattabiraman (PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over 14 years of experience publishing news analysis, research and financial product development. Connect with him via Twitter(X), LinkedIn, or YouTube. Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.

Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! ⇐ More than 3,500 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Increase your income by getting people to pay for your skills! ⇐ More than 800 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner seeking more clients through online visibility, or a salaried individual looking for a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you. (watch 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our book for kids: “Chinchu Gets a Superpower!” is now available!

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting a side income via content writing. It is available at a 50% discount for Rs. 500 only!

Do you want to check if the market is overvalued or undervalued? Use our market valuation tool (it will work with any index!), or get the Tactical Buy/Sell timing tool!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy. Freefincal is a News Media organisation dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News. Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact Information: To get in touch, please use our contact form. (Sponsored posts or paid collaborations will not be entertained.)

Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner.

Our publications

You Can Be Rich Too with Goal-Based Investing

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.Your Ultimate Guide to Travel

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)