Last Updated on October 8, 2023 at 1:32 pm

You might be wondering why the title refers to mutual fund ‘categories’. Would it not be more enticing and perhaps more useful had it read, ‘how to select mutual funds suitable for your financial goals’?

Perhaps so. However, I choose to focus on how to select mutual fund categories first, for two reasons

- I am pained to see investors select mutual funds utterly unsuitable for their goals. For example,

- selecting diversified equity mutual funds or ‘balanced’ funds with significant equity component for goals just a few years away.

- investing in volatile debt funds without understanding the risks involved.

- I strongly believe that if an investor knows how to pick the fund category suitable for her needs, the task of selecting a suitable mutual fund from that category becomes utterly simple, if not obvious.

Mutual fund returns, and associated volatility (fluctuating returns) can be evaluated in a number of ways. Trouble is very few among us take the trouble to understand these although they could be understood quite easily.

When I made a step-by-step to select a mutual fund, I used 5 of these risk-return parameters. I am delighted to note that many investors, with a near-zero experience in mutual fund investing, have started using these parameters in choosing mutual funds.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

🔥Want to create a complete financial plan? Learn goal-based investing? Exclusive access to our DIY tools? Increase your income with your skills? Enjoy massive discounts on our robo-advisory tool & courses! 🔥

In this post, let us discuss how to select a suitable mutual fund category using just one parameter: the standard deviation.

In order to understand what standard deviation is, I will borrow this wonderful analogy by Subra.

You are give two sets of numbers:

- Runs scored by Virendra Shewag in his last 25 tests.

- A similar set for Rahul Dravid

We all know how to determine the average: add up all the scores and divide by the number of such scores.

Once we get the average, we immediately recognise that some scores are higher than the average and some lower than the average.

Now if we wish to know, between Dravid and Shewag, whose scores deviate more from the average, we will need to calculate the deviation of each score wrt the average and take the average of the deviations.

This is the standard deviation. It is defined such that it is always positive so that we are not confused (assuming we are not thus far!)

Even without any data, we will recognise that Shewag is just about is capable of scoring anything from a duck to a triple hundred. Dravid on the other hand is a lot more sedate, and we can typically expect at least 30-40 runs irrespective of the conditions.

Therefore, Dravid’s scores are expected to deviate very little from the average while Shewag’s scores are expected to deviate substantially.

So we say, Dravid’s batting average has lower standard deviation than Shewag’s.

Such is the power of this analogy that it drives home the point without using any data!

Before we use the standard deviation to select a suitable fund category, let us recognise that mutual funds can be grouped together in several ways. There is no right or wrong way and each fund portal (Value Research, Morning Star, Money Control etc.) have their own categorisation scheme.

In this post, I will use the scheme categorization of VR online.

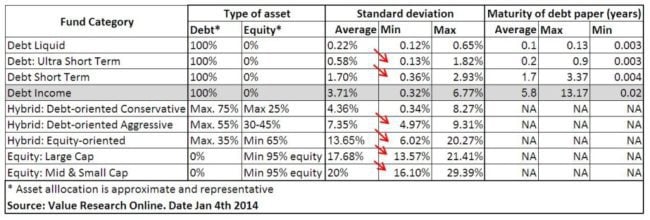

The category standard deviation, along with the typical asset allocation and maturity of debt paper (for debt funds) is listed below for some of the categories define by VR online.

Category standard deviation refers to the average standard deviation in a particular category.

Notice that returns are missing from this table.

- As you go down the table, the equity component increases. Obviously, if a fund has more equity allocation, higher would be the fluctuations in return and therefore higher the category standard deviation.

- The debt income category has different kind of debt funds (dynamic bond funds, diversified debt funds, that is funds that invest in paper that matures over different periods etc.). So it is not an exclusive group. This is why there is a huge variation in standard deviation and average maturity.

- The red arrows point to the evolution in standard deviation. The average standard deviation of one category is close to the minimum standard deviation of the next category. For the above-mentioned reason, this does not apply to income funds.

- I have not included gilt funds as they are specialised funds that resemble equity sector funds – not for everybody.

- Let us consider the first four entries that have no equity. Obviously, these are pure debt funds.

- Notice the average age at which the category debt holdings mature. A debt paper is a simple agreement between two parties: ‘I will pay an amount Y. You hold it for n days and pay me an interest r’. Of course, this is an over simplification but should suffice for our purpose.

- Liquid debt funds invest in short-term debt paper ranging over a couple of months while income debt funds invest in debt paper that can have an age of several years.

- It is clear that, higher the age of the maturity, higher is the standard deviation and therefore higher the fluctuations in returns. Of course, this also means higher returns …. typically!

Let us get to the business at hand, with a few examples.

- I have a lump sum that I wish to invest for a few months. Which fund should I choose?

I understand that equity will be too risky for just a few months. So let me eliminate all fund categories with equity.

This leaves me with the top four categories in the table.

If I choose a debt income fund that matches with the category average standard deviation of 3.71%,

My returns will typically (68% probability!!) range from

X -3.71% to X+3.71% before taxes!

Can I afford such a swing in returns?

If the answer is no, we can move on and choose somthing with lower standard deviation. What if the answer is yes?!

What if I say, I don’t mind this fluctuation?

Then you will have to worry about what X is, or what it can be.

Let us now introduce a simple but reliable rule of thumb.

- If the return(X) is greater than the corresponding standard deviation (3.70%), there is little or no chance of losing the capital invested.

- If the return is lesser than the corresponding standard deviation, chances of losing the capital invested are high.

If we adopt this thumb rule, the next question is, what is the kind of returns (X) one can expect from a debt income fund over a few months?

Well, for an income fund X should, under normal circumstances, be higher than the standard deviation.

However, as most of us realised in July this year, debts market can crash too (has happened many a time before). That is the NAV of a debt fund can sharply decrease in a day or over the course of a few weeks.

If this occurs, all debts funds are likely to be affected. Some will bounce back after a few days, some after a few weeks, and some after a few months.

If I want to invest for only a few months in a debt income fund, and if bonds crash in the period, will my fund recover?

Chances are, it will not.

I would like to use the following rule of thumb when it comes to loss of capital risk associated with debt funds.

- Longer the average maturity period, higher the corresponding standard deviation and therefore longer the time it would take for the debt fund to recover.

- If Dravid and Shewag lose form at the same time, who is likely to spring back faster? The batsman who can scratch around at the crease, or someone whose instinct is to whack every ball?

- Higher the standard deviation, bigger would be fall in the event of a crash and therefore longer it would take the debt fund to recover.

Funds with typical maturity period of more than 1 year are likely to take about 6 months to recover from a crash. I have kept track of some income funds and many are yet to recover. Unfortunately, this includes my NPS subscriptions as well 🙁

- Debt income funds are well suited only for long term goals (more than 5 years at least). Longer the period, greater is the tax advantage.

What about the other categories? How soon would they recover?

Liquid funds over a few days. Short term funds over a couple of months and ulta-short term funds a little earlier that that.

- Therefore, for investment durations of just 1-2 years stick with Short-term/Ultra-short-term/liquid funds. Fixed maturity plans (FMP) are also a good option for such durations.

What about an investment duration of 5 years?

I will choose debt funds with maturity of 1 year or less.

Why? For durations less than or equal to 5 years, the power of compounding is not that important. Therefore inflation is not that important. So I will prefer to safeguard the capital, choose debt funds of low risk.

Why not RDs or Bank FDs? If the goal is crucial and I know exactly how much I need, I will use these even if I fall in the 30% slab. If the goal is less important, then low-risk debts offer a tax advantage.

Invest durations between 5-10 years

Debt income funds that invest in debt paper of short duration with low standard deviation.

Debt-oriented Hybrid-funds with about 20-30% equity . Debt portfolio should have low maturity duration. Equity folio should have a good amount of large cap stocks. Again, both factors lead to low standard deviation (relatively!).

Invest durations above 10 years

Asset allocation should be done considering the risk profile of the goal, as beating inflation is major goal.

Now standard deviation must be high! High volatility is important for beating inflation.

Tough to choose just one fund. Perhaps if someone monitors the fund regularly, they can pull it off with a fund like HDFC Balanced. However, even for 10-year duration I would be wary of using a balanced fund like HDFC Prudence that has a high standard deviation – comparable to many large-cap equity funds!

The point of this post is to share with you how I use standard deviation to select fund categories for my financial goals.

Am I being too conservative? Am I being too risk-averse and missing out on returns?

The way I see it, for short term goals, inflation is not a major issue. So I will not risk losing capital by investing in a fund with large standard deviation.

If the asset class crashes, there will not be enough time to recover back.

For a long term goal, inflation IS the issue. So one must embrace high standard deviation, bear with short-term loss of capital and invest in mutual funds with high standard deviation. That is, those that have a good amount of equity.

Standard deviation is key to select mutual fund categories suitable for financial goals.

Would you agree?

Note: Standard deviation has some serious technical limitations. Despite that as a first step, it is good choice. I am working on suitable alternatives. Watch this space.

____________________

Ask Questions with this form

And I will respond to them in the coming weekend. I welcome tough questions. Please do not ask for investment advice. Before asking, please search the site if the issue has already been discussed. Thank you. PLEASE DO NOT POST COMMENTS WITH THIS FORM it is for questions only.

GameChanger– Forget Startups, Join Corporate & Live The Rich Life You want

My second book, Gamechanger: Forget Start-ups, Join Corporate and Still Live the Rich Life you want, co-authored with Pranav Surya is now available at AmazonOpens in a new window as paperback (₹ 199) and Kindle (free in unlimited or ₹ 99 – you could read with their free app on PC/tablet/mobile, no kindle necessary).

It is a book that tells you how to travel anywhere on a budget and specific investment advice for young earners.

The ultimate guide to travel by Pranav Surya is a deep dive analysis into vacation planning, finding cheap flights, budget accommodation, what to do when traveling, how traveling slowly is better financially and psychologically with links to the web pages and hand-holding at every step. Get the pdf for ₹199 (instant download)

You can Be Rich Too with Goal-Based Investing

My first book with PV Subramanyam helps you ask the risk questions about money, seek simple solutions and find your own personalised answers with nine online calculator modules.

The book is available at:

Amazon Hardcover Rs. 271. 32% OFF

Infibeam Now just Rs. 270 32% OFF. If you use a mobikwik wallet, and purchase via infibeam, you can get up to 100% cashback!!

Flipkart Rs. 279. 30% off

Kindle at Amazon.in (Rs.271) Read with free app

Google PlayRs. 271 Read on your PC/Tablet/Mobile

Now in Hindi!

Pre-order the Hindi version via this link

🔥Enjoy massive discounts on our courses, robo-advisory tool and exclusive investor circle! 🔥& join our community of 7000+ users!

Use our Robo-advisory Tool for a start-to-finish financial plan! ⇐ More than 2,500 investors and advisors use this!

Track your mutual funds and stock investments with this Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds and ETF screeners and momentum, low-volatility stock screeners.

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalized investment advice. We can write a detailed article without mentioning your name if you have a generic question.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

About The Author

Dr M. Pattabiraman(PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over ten years of experience publishing news analysis, research and financial product development. Connect with him via Twitter(X), Linkedin, or YouTube. Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free investment advice.

Dr M. Pattabiraman(PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over ten years of experience publishing news analysis, research and financial product development. Connect with him via Twitter(X), Linkedin, or YouTube. Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free investment advice.Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! ⇐ More than 3,000 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition is!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Our new course! Increase your income by getting people to pay for your skills! ⇐ More than 700 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner who wants more clients via online visibility or a salaried person wanting a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you! (watch 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our new book for kids: “Chinchu Gets a Superpower!” is now available!

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting side income via content writing. It is available at a 50% discount for Rs. 500 only!

Do you want to check if the market is overvalued or undervalued? Use our market valuation tool (it will work with any index!), or get the Tactical Buy/Sell timing tool!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy. Freefincal is a News Media Organization dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News. Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact information: To get in touch, use this contact form. (Sponsored posts or paid collaborations will not be entertained.)

Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner.

Our publications

You Can Be Rich Too with Goal-Based Investing

Published by CNBC TV18, this book is meant to help you ask the right questions and seek the correct answers, and since it comes with nine online calculators, you can also create custom solutions for your lifestyle! Get it now.

Published by CNBC TV18, this book is meant to help you ask the right questions and seek the correct answers, and since it comes with nine online calculators, you can also create custom solutions for your lifestyle! Get it now.Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

This book is meant for young earners to get their basics right from day one! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.

This book is meant for young earners to get their basics right from day one! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.Your Ultimate Guide to Travel

This is an in-depth dive into vacation planning, finding cheap flights, budget accommodation, what to do when travelling, and how travelling slowly is better financially and psychologically, with links to the web pages and hand-holding at every step. Get the pdf for Rs 300 (instant download)

This is an in-depth dive into vacation planning, finding cheap flights, budget accommodation, what to do when travelling, and how travelling slowly is better financially and psychologically, with links to the web pages and hand-holding at every step. Get the pdf for Rs 300 (instant download)