Last Updated on December 29, 2021 at 12:12 pm

Gilt mutual funds are those that predominantly invest in government bonds (gilts).For a citizen, such bonds carry no credit risk, that is the risk of perceived or actual delay or default in interest payment*. However, this brings to the table a new of problems that investors need to know of. If you cannot stomach the possibility of credit risk in debt mutual funds, here is how you can use gilt mutual funds

* Gilt mutual funds are classified by rating agencies as “sovereign risk”.Internationally, the bonds of one country can be compared with another and a credit rating is assigned. For example, Moody’s current long term sovereign rating of Indian bonds is Baa2 with a stable outlook. This is 8 notches below AAA, but still considered investment grade.

In fact, India was arm twisted into opening its economy in the early nineties when it was on the verge of bankruptcy. Government bonds were near junk demanding 12% ish interest rates (EPF and PPF were hovering around this). So although it is technically incorrect to say gilts do not have credit risk, practically, for a citizen it is not of everyday relevance. If the government is unable to repay its debt to citizens, all of us will have much bigger problems to worry about than the fall in NAV of our debt mutual funds and who said what on Twitter.

🔥Secure your future with our Robo-advisory tool trusted by over 3,000 investors and advisors. From effortless retirement planning to funding your children’s biggest dreams, turn your financial goals into reality. 🔥

Subscribe for money management solutions via email! (Link takes you to our email sign-up form) Join 32,000+ readers in our community.

👉 New Tool Alert! NaviPlan: A Privacy-Focused Multi-asset Tracker and Goal Planner 👈

Gilt mutual funds: Positives for the investor

- No credit risk.

- Suited for long-term goals as fixed income component, but periodic rebalancing is essential to reduce risk and lock in gains.

Gilt mutual funds: Negatives for the investor

Wait a minute.Just two positives? That is it? Depending on how you look it, that is a lot or that is it. Let us understand this better by looking at the negatives.

- Cannot be used for short-term goals ( less than 5 years) or for simply parking money. Short term gilt funds can be used but they are not longer available after the SEBI categorization rules

- Daily volatility will become significantly higher when compared to liquid or ultra short term funds. Shown below is the NAV of SBI contant maturity gilt fund. The fund was converted from a short term gilt to a 10Y gilt fund due to SEBI rules. You can literally tell when the fund changed by looking at the NAV.

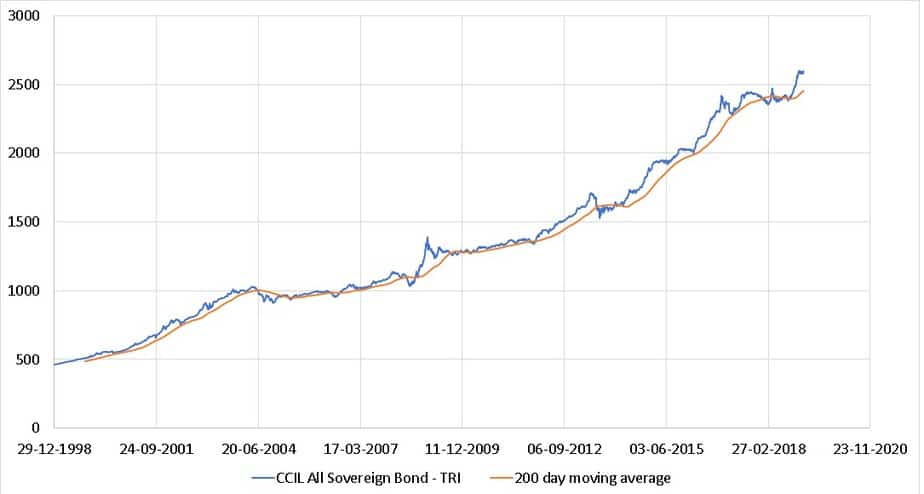

- There will be months of month of low or even negative returns where the NAV stays “under water” (below a past maximum). Are people who complain about credit risk ready to face this prospect without complaining or feeling worried? I doubt it. The 200 day moving average of CCIL All Sovereign Bond – TRI is shown below. Notice that the NAV can be below its 200 day moving average for months (ignore the movement in the early 2000s when it was below for years!).

While such dips present a buying oppurunity, it also means past returns would be erased. It is one thing if it happens in equity and quite another in “fixed income”. So tread with caution.

- While credit downgrades are like Earhquakes where the NAV falls vertically down. gilt fund NAVs are more like soil erosion or deforestraion where the change is gradual and visible but not too sudden. To assume the latter is better than the former is folly.

- AUM is a problem and choices are limited. In the 10Y gilt category where the fund only invests in 10-year bonds. Only one fund (the above SBI fund) has a reasonable AUM of 359 croes. All others have less than one tenth of that AUM!! In the normal gilt category, only three funds have a 1000+ crore.

- Gilt funds can only be used for goals five years or more away. Even then, just like equity, one will have to remove money gradually or in one shot well before the goal else if there is a rate hike just before the goal deadline, there will be losses. So the tax efficiency of gilts are lower than other debt funds.

So are the negatives more than the positives? If you consider investor mentality, choosing gilts over other types of debt funds can be a case of jumping from the frying pan into the fire. I think investors are better off with lage AUM lilquid funds if they are worried about credit risk.

I would like to use gilt funds. How should I go about it?

The first thing to understand is you cannot eat your cake and have it too. You cannot get rid of one type of risk and then expect the gilt fund to give you good returns. Since there are no short term (<1Y) gilt funds anymore, you simply cannot expect anything from a gilt fund. There is too much volatility.

Of course, the same is true of any debt fund, but in the absence of credit risk, it is reasonable to expect something. The only problem (and a big one at that) is finding a non-gilt fund with low credit risk. Well my point is, just because credit downgrades are taken off, does not mean the fund is safe and you can expect a return. Time value of money plays a big role in medium and long term gilts. That is the NAV can keep moving down or nowhere for weeks to months.

You can only use them for medium to long term goals, preferably long term like retirement. You have two choices:

- The 10Y gilt fund will be a lot more volatile then normal gilt funds but there will be not fund management risk. If you wish to actively rebalance between equity and debt depending on gains then this would be a good choice

- All other gilt funds will behave like dynamic bond funds trying to move from short term to long term gilts depending on market supply and demand. They can get it right or wrong, but the day to day volatility will be lower than the 10Y gilt funds. If you want some amount of active management with yearly or occasional rebalancing, this would be a good choice.

Ideally gilt funds are supposed to fall when equity moves up and vice versa so that tactical asset allocation is possible. This happended during the pre-2008 bull run, but not since (not for substantial periods). So one cannot count on this. The bottom line however is, gilt investors should either periodically move in and out or face the music if they buy and hold. To assume credit free risk options are better is folly.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email!(Link takes you to our email sign-up form)

Use our Robo-advisory Tool to create a complete financial plan! More than 3,000 investors and advisors use this! Use the discount code robo25 for 20% off. Plan your retirement (early, normal, before, and after), as well as non-recurring financial goals (such as child education) and recurring financial goals (such as holidays and appliance purchases). The tool would help anyone aged 18 to 80 plan for their retirement, as well as for six non-recurring and four recurring financial goals, with a detailed cash flow summary.

🔥You can also avail massive discounts on our courses and the freefincal investor circle! 🔥 & join our community of 8000+ users!

Track your mutual funds and stock investments with our Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds, ETF screeners, as well as momentum and low-volatility stock screeners.

You can follow our articles on Google News

We have over 1,000 videos on YouTube!

Podcast: Let's Get RICH With PATTU! Every single Indian CAN grow their wealth!

You can watch podcast episodes on the OfSpin Media Friends YouTube Channel

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalised investment advice. We can write a detailed article without mentioning your name if you have a generic question.

About The Author

Dr M. Pattabiraman (PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over 14 years of experience publishing news analysis, research and financial product development.

Connect with him via Twitter(X) LinkedIn YouTube

Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! More than 3,500 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Increase your income by getting people to pay for your skills! More than 800 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner seeking more clients through online visibility, or a salaried individual looking for a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you. (Watch the 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our book for kids: “Chinchu Gets a Superpower!” is now available!

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.

Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting a side income via content writing. It is available at a 50% discount for Rs. 500 only!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy

Freefincal is a News Media organisation dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News.</p river> Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact Information: To get in touch, please use our contact form. (Sponsored posts or paid collaborations will not be entertained.)Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner

Our publications

You Can Be Rich Too with Goal-Based Investing

Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

Your Ultimate Guide to Travel