Last Updated on August 30, 2021 at 4:19 pm

Many debt mutual funds invest in corporate bonds which carry credit risk. It is important for investors to understand how this can affect debt mutual fund returns.

Yesterday, rating agencies, CRISIL, ICRA and CARE downgraded short-term and long-term ratings on Jindal Power and Steel bonds.

As a result, the NAV of debt funds which held Jindal bonds fell. Have a look at this summary by Manoj Nagpal.

Bad NAVs of debt funds are back!

Impact of downgrade of JSPL on debt fund NAVs today pic.twitter.com/6y6PMZCSOh— Manoj Nagpal (@NagpalManoj) February 16, 2016

🔥Secure your future with our Robo-advisory tool trusted by over 3,000 investors and advisors. From effortless retirement planning to funding your children’s biggest dreams, turn your financial goals into reality. 🔥

Subscribe for money management solutions via email! (Link takes you to our email sign-up form) Join 32,000+ readers in our community.

👉 New Tool Alert! NaviPlan: A Privacy-Focused Multi-asset Tracker and Goal Planner 👈

This fall is not of the same magnitude as the fall in JP Morgan funds (see below). This rating downgrade is also different in nature. I think investors can continue to hold Franklin Templeton funds. Unlike Amtek Auto, I think Jindal Steel should be able to pay back the principal to FT when the bond matures. The NAV fall was only a market-linked fall. FMP returns will be lower.

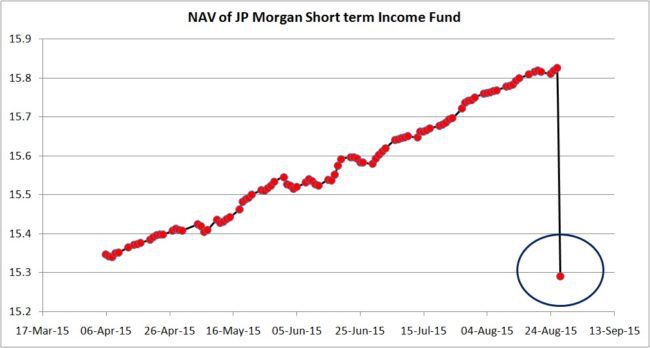

This is the second time in six months we see such a fall in debt funds. In Aug 2015, JP Morgan AMC was in the news for the wrong reasons. The NAV of two of its debt mutual funds, JP Morgan Short Term Income Fund and JP Morgan India Treasury Fund fell by -3.38% and – 1.73% on Aug. 27. The reason: both funds held debentures (bond) of Amtek Auto which was downgraded from AA- to C.

Impact of credit crisis in Mutual Funds on Franklin Templeton Debt AUM

AUM down 15k+ cr (30% of Aug15 AUM) pic.twitter.com/tcz5xSnRZN— Manoj Nagpal (@NagpalManoj) February 17, 2016

A look at how credit rating changes affect debt mutual funds.

Categories of debt mutual funds can appear difficult to understand than that of equity mutual funds. There is a simple way for investors to understand the risks associated with different debt mutual fund categories – the modified duration.

As pointed out in previous posts, the modified duration is measured in years and gives us two pieces of information:

- For 1% change in interest rates, what would be the expected increase or decrease in fund NAV. A modified duration of 2 years implies, a possible NAV change of 2% for 1% change in interest rate. So longer the modified duration, higher the interest rate sensitivity.

- For a given yield to maturity, how long would the fund take to recover, if there is a loss due to increase in interest rates.

The key to understanding credit rating risk is to recognise that credit risk does not refer to risk of default alone (bond issuer does not pay interest). Since debt mutual funds are marked to market, any change in credit rating will affect the price of the bond and therefore, the NAV of the fund.

There are two types of interest rate changes that affect the NAV:

1) RBI action on short-term interest rates which will impact long-term rate of GOI bonds and corporate bonds as well.

2) Change in credit rating of a corporate bond.

Many investors are under the misconception that corporate bond opportunity funds are immune to RBI action. This is incorrect. Corporate bonds carry a risk premium (higher interest rate) with respect to GOI bonds which will change when the GOI bond rates change.

Due to this risk premium, Corporate bonds must be graded as per their perceived ability to repay the principal. This is referred to as a credit rating.

Higher the credit rating, higher the faith in the company and lower the risk of default.

Now if the credit ratings go up for a bond, the interest rate of the bond in the market will decrease. Therefore, the value of the bonds the fund currently held by the fund will be worth more than those in the market. Thus, the NAV of the fund will sharply increase.

Conversely, if the credit ratings go down for a bond (like it did for Amtek Auto), the interest rate of the bond in the market will increase. Therefore the value of the bonds held by the fund will be worth less, and the NAV will drop sharply.

In either case, as long the firm repays the principal to the fund, the NAV over time will gradually get back to the normal linear movement.

If you wish to calculate how long it would take for the recovery (in case of a credit rating downgrade), you can consult this post: Understanding Interest Rate Risk in Debt Mutual Funds

However, if the firm defaults then the loss is permanent (thanks to Mahesh Mirpuri for clarifying this).

Therefore, due to fear of default a debt fund, in this case the above-mentioned funds, may face redemption pressure.

If you wish to choose debt funds that invest in corporate bonds, I suggest you choose funds with low modified duration (much less than one year). So even if there is a downgrade in credit rating, the loss (assuming no default) can be recouped in a couple of months.

You can minimise such risks by using the so-called Banking and PSU debt mutual funds. They invest in bond issued by PSUs and banks only.

To lower credit risk and interest risk, I would shun every other debt fund category except ultra short-term funds and liquid funds. See why here: Investing in debt mutual funds: slow and steady wins the race!

Another read on the subject: How to Select Debt Mutual Funds Suitable For Your Financial Goals?

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

🔥You can also avail massive discounts on our courses and the freefincal investor circle! 🔥& join our community of 8000+ users!

Track your mutual funds and stock investments with this Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds, and ETF screeners, as well as momentum and low-volatility stock screeners.

You can follow our articles on Google News

We have over 1,000 videos on YouTube!

Join our WhatsApp Channel

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalised investment advice. We can write a detailed article without mentioning your name if you have a generic question.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

About The Author

Dr M. Pattabiraman (PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over 14 years of experience publishing news analysis, research and financial product development. Connect with him via Twitter(X), LinkedIn, or YouTube. Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.

Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! ⇐ More than 3,500 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Increase your income by getting people to pay for your skills! ⇐ More than 800 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner seeking more clients through online visibility, or a salaried individual looking for a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you. (watch 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our book for kids: “Chinchu Gets a Superpower!” is now available!

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting a side income via content writing. It is available at a 50% discount for Rs. 500 only!

Do you want to check if the market is overvalued or undervalued? Use our market valuation tool (it will work with any index!), or get the Tactical Buy/Sell timing tool!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy. Freefincal is a News Media organisation dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News. Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact Information: To get in touch, please use our contact form. (Sponsored posts or paid collaborations will not be entertained.)

Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner.

Our publications

You Can Be Rich Too with Goal-Based Investing

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.Your Ultimate Guide to Travel

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)