Last Updated on December 28, 2021 at 6:35 pm

This week on fee-only advisor journey, we showcase Swapnil Kendhe’s successful transition from corporate executive to insurance and mutual fund salesman to a fee-only SEBI registered investment advisor (RIA). Swapnil is part of both fee-only India – an association of fee-only financial planners and the freefincal list of fee-only RIAs.

As someone who has witnessed part of this transition and how Swapnils thought process changed in favour of fee-only advisory, I am immensely proud to present his journey to you. It is one thing to listen to your calling and follow it, but quite another to abandon a lucrative income source to do so. Swapnil not only got rid of his mutual fund distribution but also made sure he switched his regular plan customers to direct plans once he embraced fee-only advisory. There was no need for him to do so as SEBI regulations permit old commissions to continue, but that was not acceptable to him.

Not only is he an honourable, ethical person, he is one of the few people in the financial services community who does not take past performance seriously and gives risk management the priority that it deserves. Naturally, I find that attitude and his willingness to push himself and learn new things endearing.

You can contact Swapnil via his website: Vivektaru. Now over to him.

🔥Secure your future with our Robo-advisory tool trusted by over 3,000 investors and advisors. From effortless retirement planning to funding your children’s biggest dreams, turn your financial goals into reality. 🔥

Subscribe for money management solutions via email! (Link takes you to our email sign-up form) Join 32,000+ readers in our community.

👉 New Tool Alert! NaviPlan: A Privacy-Focused Multi-asset Tracker and Goal Planner 👈

“Past events always look less random than they were. I would listen to someone’s discussion of his own past realising that much of what he was saying was just a backfit explanation concocted ex post by his deluded mind.” -Nassim Taleb in the preface of his book Fooled by Randomness.

While the temptation is always there to present a better-looking picture of your own past (based on your memory of the past which is slightly different from what you experienced in reality), I have tried to tell my story like it is.

I have no formal education in personal finance and investing. I accidentally landed in this profession which luckily suited me. What follows is majorly the story of how I learned personal finance starting as an insurance agent.

I am a Chemical Technologist by education. I worked with Marico Ltd. and Hindustan Unilever Ltd. as production executive for 3 years. In 2011, I left the job to do something of my own and started a business. Business did not work as expected and I had to close it within a year. This left me in debt and with no cash flow.

In mid-2012, when I had nothing else to do, I applied for LIC agency on a friend’s suggestion. I wanted a temporary source of income until I find something worthwhile to do. But things changed during 10 days of mandatory training before IRDA exam. I heard stories of successful insurance agents and huge income they earn. Incidentally, one of India’s Biggest Insurance Agents Bharat Parekh has an office in the same building I attended this training in. This changed my perception of the profession of Insurance selling and I decided to take it seriously.

I got my LIC licence in Aug 2012. I began attending agent training, purchased LIC agent software, and spent days studying plans and plan combinations. Like all LIC agents, I also believed that there is no better investment option than LIC.

At around the same time, someone suggested that if anyways I am selling insurance, why sell products of one company when it is possible to sell any insurance company’s product through insurance brokers like Bajaj Capital. So I empanelled with Bajaj Capital in Sep 2012 and began selling all types of insurances through them. In health insurance, I used to sell Apollo Munich and Max Bupa policies.

Company Fixed Deposits could also be sold through Bajaj Capital, but I never sold them. Quite a few Company Fixed Deposits sold by Bajaj Capital like Plethico Pharma, Elder Pharma, Bilcare, Unitech, Jaiprakash Associates, Omnitech, Micro Technologies have defaulted. I was lucky not to have touched them.

I also took Oriental agency specifically to sell ‘Oriental Happy Family Floater’. This product used to beat all other health insurance products in premium especially if older members of the family were covered in a family floater policy. There was a flaw in the design of this product and oriental subsequently corrected it.

Barring few close friends, I did not approach friends, relatives and acquaintances to sell insurance since it was embarrassing for me to be seen selling insurance after leaving a good job at HUL. I acquired almost all my early clients through cold calling and subsequent clients through references. I have not asked for references myself from any of my clients all these years. I am too proud to do that (not sure if it is a virtue or vice).

This was a terrible way to sell insurance. My commission in those early days would not even cover EMI of the personal loans I had taken for my sister’s marriage and renovation of our ancestral house.

One fine day I stumbled upon Jagoinvestor.com and it opened a real world of personal finance for me. I learned about the inferiority of traditional insurance products for the first time on Jagoinvestor. I also discovered subramoney.com in one of the reader comments there.

Subramoney was a treasure trove of personal finance wisdom. It was addictive. For next few days, I was reading Subramoney leaving everything else. It transformed me from an average insurance agent to a decent adviser within few days. I have been a regular reader of Subramoney since I discovered it in 2013. I read all Subramoney articles published from 2008. I wanted to see what Subramoney had to say when 2008 market crash was actually happening. I started with the first article published in 2008 and kept reading subsequent articles. By the time I stopped, I had reached the end of 2011.

I became a Mutual Fund distributor in mid-2013. I was a regular reader of Jagoinvestor.com during this period. There was this man Ashalanshu all over Jagoinvestor that time. He used to comment on almost every query. In the 2nd half of 2013, Ashalanshu’s activity began going down on Jagoinvestor. When I asked him about it in one of my comments, he replied that he is busy with his own Facebook group. I asked if I could join his group and he added me to Asan Ideas for Wealth(AIFW).

AIFW in those days was amazing. I had already discovered freefincal.com by then and was using freefincal calculators. Pattabiraman Murari of freefincal.com was active on AIFW and so was P.V. Subramanyam of subramoney.com. Some quality DIY (Do It Yourself) investors, as well as many well established financial advisers, were equally active on the group. My reading and learning of personal finance and investing had already picked up speed by the time I landed on AIFW. But it was mostly through books and blogs. AIFW added the much-needed human element to it.

My participation in AIFW discussions was totally devoid of political correctness. It irked few people but also attracted the attention of right kind of people like Pattabiraman Murari and Ashal Jauhari (I was less aware of my ignorance that time and therefore would post, comment and participate in discussions more often).

Sometime at the end of 2013, Pattabiraman Murari shared with me Canada based financial adviser Jim Otar’s book “Unveiling the retirement myth”. This book has influenced the way I look at financial planning more than anything else. I learned to look at financial planning in terms of lucky and unlucky outcomes because of this book. It also made me aware of the sequence of return risk which is one of the most important factors to be considered while doing financial planning.

I discovered Nassim Taleb on Subramoney. Since I did not have spare money to buy books in those days, my reading was restricted to free e-books I could download from internet (all my income would go towards loan EMIs and paying off debt I had incurred because of my failed business).

Reading Taleb was like getting trained in inference. Taleb made me sceptical of all self proclaimed experts (investing is all about future and those we call expert are as clueless about the future as we are). He made me doubt the quality of my own knowledge too. I began understanding the role luck plays in investment performance. My understanding of risk also became better with Taleb.

Reading, studying and exploring personal finance and investing had become the principal activity of my life by this time. Subramoney.com has a list of 57 must-read investment books. I have 33 of these books in my personal library of close to 100 investment and related books. I have read most of these books, partially read some and reread few many times. Reading a book or blog is like entering a room. It opens doors to other rooms. I have a habit of opening every door I see and checking the adjacent room. Poor Charlie’s Almanack is one room I never get tired of spending time in. Charlie Munger’s approach of “trying to be consistently not stupid instead of trying to be very intelligent” better suits my temperament. This is also the way I like to handle financial planning.

Twitter has also been a great source of learning for me. Whenever I discover some quality handle like @contrarianEPS, I usually read all the past tweets, check other handles it follows and add good handles to different lists I maintain on twitter. Twitter has also become my primary source of news since I do not read newspapers and watch TV.

In my early days in this profession, I wanted to do CFP (Certified Financial Planner) but the cost of CFP was too high for me that time. By the time I came in a position to afford it, I had already explored quite a bit of personal finance. I had also seen many advisers flaunting their CFPs whose understanding of personal finance I was not impressed with. If CFP and other such certifications (textbook learning to pass exams) were not going to make me a better adviser, then acquiring them only for image building to attract more business was unethical. By the same token, SEBI RIA is one more decoration that tells nothing about the competence of an adviser.

I stopped selling LIC policies shortly after landing on AIFW which lead to the termination of my LIC agency. I also transferred my health insurance business to one senior health insurance agent in Nagpur who deals exclusively with health insurance. I did not have experience of handling claims and my clients could be better served by this agent. I also wanted to get out of insurance completely because Mutual fund used to excite me more than insurance. This gave me more time to explore personal finance and investing.

I was a member of AIFW when SEBI came up with RIA (Registered Investment Advisor) regulation in 2013. There used to be animated discussions in AIFW about this regulation that time. Initially, I was on the side of adviser community ridiculing Fee Only model but slowly I realised that this is a far superior model from the point of view of investors.

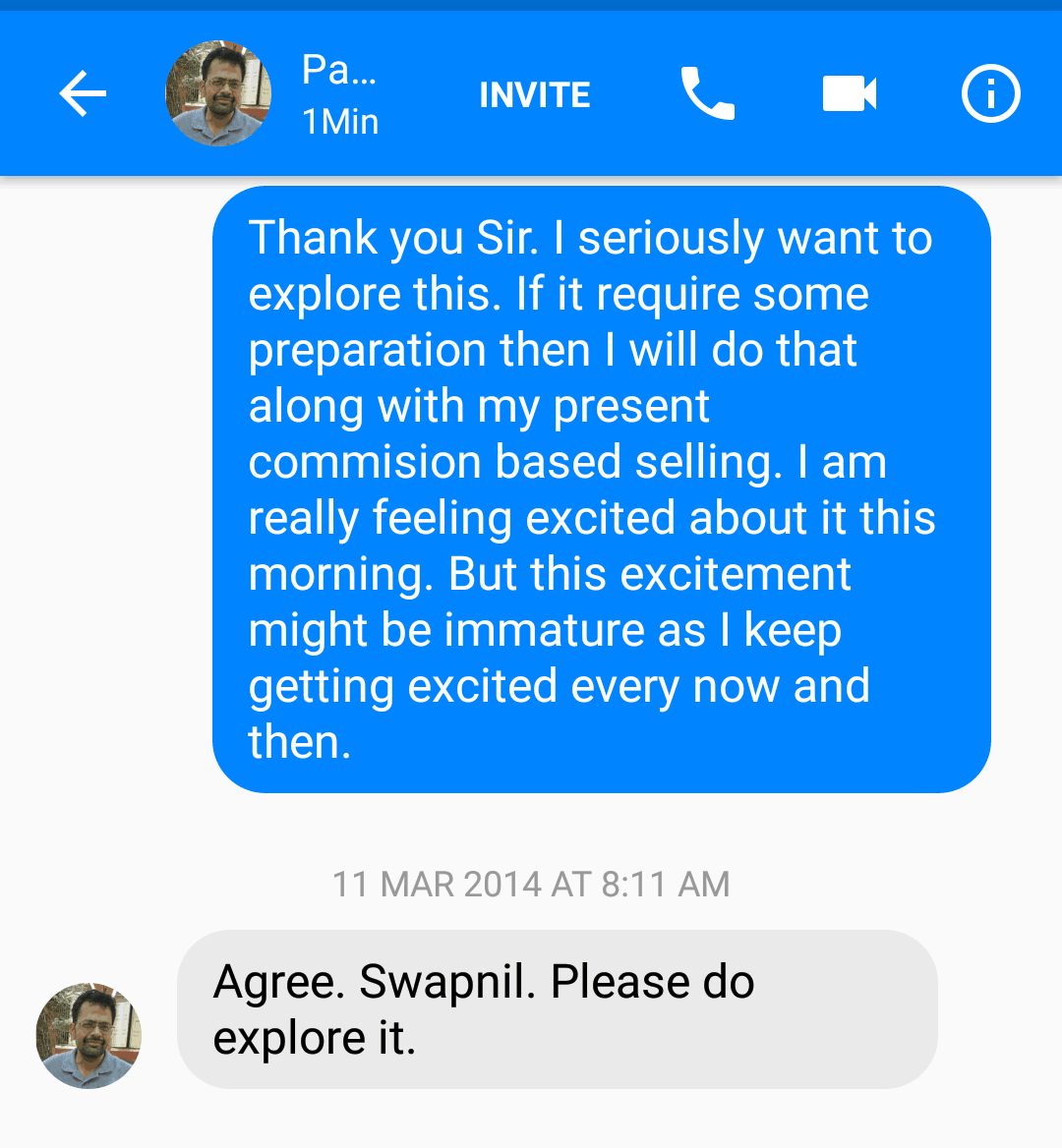

This was my message to Pattabiraman Murari dated March 11, 2014 by which time, I had begun thinking seriously about moving to fee-only model. Since I did not have post-graduate degree in finance, I needed to fulfil 5-year minimum experience criteria to apply for RIA registration which was still three and half years away. I decided to use this time to build my competence as a financial adviser.

This was also the time when I began staying away from IFA (Independent Financial Adviser) community. Most IFAs have a tendency to think in terms of Mutual Fund AUM, size of SIP book, number of clients and commission. Rarely have I come across an IFA who works as much on sharpening his knowledge of Investing as he does on increasing his income. This is the obvious outcome of a system that appreciates and pays to do more not better.

Prospects of earning a higher income somehow does not excite me (This has something to do with my constitution I guess. I wanted to join Ramakrishna Mission when I was in college and even when I was doing a job). I had no appetite for doing 3-5 client/prospect meetings every day either (I am lazy when it comes to doing non-intellectual work). I also have an inability to offer my clients one option when I am aware of a better option is available for them. I struggled with not talking about direct plans of mutual funds for a long time and stopped putting my clients’ money in regular plans even before becoming an RIA. I was a misfit in IFA community where nobody believed in a fee-only model. My reclusion from IFA community helped me in keeping my thinking clean and maintaining my conviction in the fee-only model.

I do not want to take moral high ground here for my decision to move to fee-only model because it was also a rational decision for me to take. AUM gathering (selling) was a game I had little aptitude for and even if I had tried, I could not have become a top IFA; but I can definitely make a name for myself as an RIA.

In mid-2016, one of my clients asked me to recommend few good stocks for his stock portfolio. I was not comfortable doing this but when he kept insisting, I asked him a couple of month’s time to do the study. For next 3 months, I explored direct equity leaving everything else. I kept doing the same for 3 more months after giving my recommendations. In early 2017 I had to take responsibility of the stock portfolio of one more of my clients against my will. Once again I found myself spending all my time doing direct equity research. I was also handling my brother in law’s stock portfolio during this time and equity portion of my personal portfolio was also totally invested in stocks. Being a bull market all these portfolios did well. This consumed more than 80% of my time for close to a year. Though I did not earn anything for all this work, it further increased my understanding of equity as an asset class.

My father had helped me close my personal loans and part of debt from his retirement proceeds at the end of 2015 but I still had some money to be returned to a couple of my close friends. In the 2nd half of 2017, I sold my stock portfolio to clear all my debt and to construct my office at home. After selling my own stock portfolio, I noticed that I had lost the intensity with which I was doing stock research earlier. I was also about to submit my RIA application and I knew that I will not get enough time to do justice to direct equity advice. I did not think that I have knowledge, competence and experience enough to advice on direct equity either.

So I sold direct equity portfolio of my brother in law I was handling. My first direct equity client had already sold his portfolio for his house construction. I approached the other client and told him that I will not be able to take responsibility for his direct equity portfolio. I suggested him either to sell his stock portfolio and invest the amount in a mutual fund or take the advice of some competent adviser who can take responsibility of his stock portfolio. This got him angry but he did as suggested. He was in good profit and since I had not charged him anything, there was no obligation on my part.

I cleared mandatory exams for SEBI RIA registration in Feb-2017 and applied for registration after my 5-year minimum experience criteria got fulfilled in Aug 2017. I got my registration on Oct 31, 2017.

I had not yet received my registration when I attended the first meeting of Fee Only India (FOI) in Sept 2017. A month before this meeting, I had spent a day with Melvin Joseph of finvin.in when he had come to Nagpur to deliver a guest lecture in one MBA college. Melvin Joseph was the first man I met from adviser community I felt completely at ease with. I have always found it difficult to speak my mind with most people in this profession. Either they find me over smart or impractical (some call me plain stupid). With Melvin Joseph, I didn’t have to dilute my talk. He was also willing to share everything with advisers ready to work on clean fee-only model.

I had a similar experience with other members of FOI. It feels like family in FOI. Ashal Jauhari and Pattabiraman Murari are like the binding force for the group. I also cherish the privilege of discussing difficult financial planning cases with Ashal Jauhari and intellectual stuff with Pattabiraman Murari.

This is one profession where experience does count. I have tried to compensate my lack of experience by spending the majority of my time studying and exploring personal finance and investing in last 5 and half years but I only had as much time. There are still many things I need to learn to fluency as a financial adviser. I have also realised that I cannot become expert at everything.

I do not want to work as an adviser in an area where my knowledge is superficial. Financial planning of resident Indians falls within my circle of competence and I want to stick to it as of now. I do not want to handle NRI clients since I do not have enough grasp of applicable taxation and investment options available for them outside India. I no longer provide stock recommendations either.

My wife resigned from her job (as we had decided) the very next day I got my registration and got relieved from the job in 2nd week of Dec. She was working as a teacher in one private school in Nagpur. We are twa o-member team now. We provide all services IFAs provide to our local clients in addition to the unbiased commission-free advice. The fee is for my availability for a year and not only for financial planning. Since I was a full time mutual fund distributor before becoming an RIA, I have established client base of more than 100 clients. We are moving our existing clients to fee only model. In last 4 and half months after my RIA registration, we have handled 27 financial planning clients; 5 of these clients are online clients.

Financially it is more rewarding for advisers to work with well to do clients. But I want to offer my services to lower income section of the society as well because their need for financial hand holding is perhaps higher than well to do members of the society. Since they cannot afford my financial planning fee, I charge them consultation fee and help them get insurances and invest in mutual funds. I have no set fee structure for such consultation.

It is popular opinion within adviser community that fee-only model doesn’t work in India but this model better suits my temperament and it is working fine for me.

=-=-=-=-=-=

If you wish to work with Swapnil, contact him via his website: Vivektaru.

This article was first published on his website: My story

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

🔥You can also avail massive discounts on our courses and the freefincal investor circle! 🔥& join our community of 8000+ users!

Track your mutual funds and stock investments with this Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds, and ETF screeners, as well as momentum and low-volatility stock screeners.

You can follow our articles on Google News

We have over 1,000 videos on YouTube!

Join our WhatsApp Channel

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalised investment advice. We can write a detailed article without mentioning your name if you have a generic question.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

About The Author

Dr M. Pattabiraman (PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over 14 years of experience publishing news analysis, research and financial product development. Connect with him via Twitter(X), LinkedIn, or YouTube. Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.

Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! ⇐ More than 3,500 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Increase your income by getting people to pay for your skills! ⇐ More than 800 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner seeking more clients through online visibility, or a salaried individual looking for a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you. (watch 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our book for kids: “Chinchu Gets a Superpower!” is now available!

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting a side income via content writing. It is available at a 50% discount for Rs. 500 only!

Do you want to check if the market is overvalued or undervalued? Use our market valuation tool (it will work with any index!), or get the Tactical Buy/Sell timing tool!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy. Freefincal is a News Media organisation dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News. Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact Information: To get in touch, please use our contact form. (Sponsored posts or paid collaborations will not be entertained.)

Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner.

Our publications

You Can Be Rich Too with Goal-Based Investing

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.Your Ultimate Guide to Travel

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)