Last Updated on December 29, 2021 at 6:21 pm

A reader asks, “Had watched many of your videos on asset allocation. I have a question in mind for which maybe I don’t have proper data to back it up. Example: In my case, let’s says I started investing at the age of 26-27and. I have saved enough money for short term goals.”

“All my future goals are of 15+ year duration, should I just not put 100% in equity index funds and try to accumulate more units in early age to make a good corpus and maybe in future try to add more debt to portfolio once age increase.

Why maintain a 60:40 ratio, instead start with 100 and maybe end with 50:50. Please throw some data and your analysis”.

First of all, this quote from the movie Lawrence of Arabia often reminds me not to dismiss young investors’ opinions.

Young men make wars, and the virtues of war are the virtues of young men: courage, and hope for the future. Then old men make the peace, and the vices of peace are the vices of old men: mistrust and caution. – Lawrence of Arabia (1962)

Second of all, we must appreciate the assumptions made by the reader in forming this opinion. He assumes accumulating more units early in the investment journey will result in a higher corpus or more returns. This is incorrect. As shown earlier, returns from equity over the long-term still fluctuate quite a bit, and we do not know what return we would get: Do not expect returns from mutual fund SIPs! Do this instead! And What return can I expect from a Nifty 50 SIP over the next 10 years?

🔥Secure your future with our Robo-advisory tool trusted by over 3,000 investors and advisors. From effortless retirement planning to funding your children’s biggest dreams, turn your financial goals into reality. 🔥

Subscribe for money management solutions via email! (Link takes you to our email sign-up form) Join 32,000+ readers in our community.

👉 New Tool Alert! NaviPlan: A Privacy-Focused Multi-asset Tracker and Goal Planner 👈

So whatever asset allocation you use, returns from equity will always be uncertain. That is why we keep urging readers to build a goal-based strategy that goes beyond returns.

The “standard” 60% equity and 40% fixed income or 50% equity and 50% fixed income is only a reference to the initial portfolio asset allocation. How an investor achieves a corpus close to or preferably above the target corpus entirely depends on how they vary this asset allocation.

So there is no magical asset allocation mix that would “work”. Portfolio management, like marriage, has to be worked on continuously. The reader wants to know the efficacy of a “start with 100% equity and maybe end with 50:50” strategy with data.

We will consider a 20-year goal and set the following asset allocation schedule. The saw-tooth like pattern in the graph below represents annual rebalancing.

- 100% Equity for 10 years

- 60% equity for next 5 years

- 0% equity for next 5 years

We will use 660 monthly S&P 500 TRI and 1Y US Treasury bill index returns and backtest it over 421 possible 20-year return sequences with the above asset allocations. We will be ultra-conservative wrt return expectations and assume only 5% expectation from the S&P 500 TR (not this is for a US investor!) and only 0.8% return from the 1Y T-bill index. These are well below historical averages.

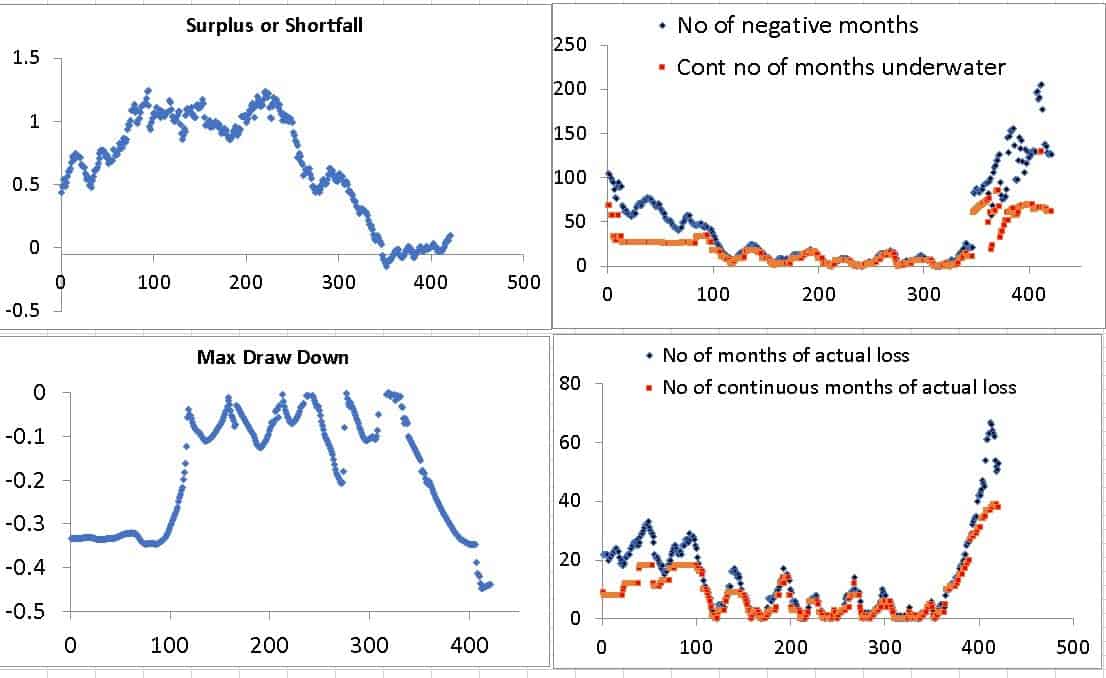

The results are summarized in the four graphs below.

- Top left: If the surplus is positive, the final corpus > target corpus. A hopeful investor might see all those trials when the strategy was a success. A cautious investor would see that not all trials were successful, and the success margin varied quite a bit.

- Top Right: No of months the corpus was < target corpus and no of months the corpus was continuously < target corpus. Again the hopeful investor would look at the no of trials when these were low, and the cautious investor would look at the trials when the corpus was < target corpus for years!

- Bottom left: The max negative deviation from the target portfolio: 20-30% or even more is routinely seen.

- Bottom right: Total no of months of negative portfolio returns and continuous negative returns.

Please note no probability can be derived from the above results. As market conditions keep varying, a strategy can fail more or win more. They say that we cannot backtest emotions. We can if we are emotional about being open-minded and look for the risk.

Will a 100% equity initial allocation strategy work? Yes, but not all the time. Will a 60% equity and 40% fixed income and equity tapered to zero in the last three years (which many “advisors” recommend so that commissions are maximised) work? Sometimes yes, sometimes no.

Can I use 70% or 80% equity for the first few years? The reasoning is just the same. Sometimes it will work, and sometimes not. The point is, investing more into equity is not a guarantee of success.

No strategy will work all the time. The question is, will you rely on plain hope that it will work sometimes and choose a plan where the margin of both success and failure (measured wrt deviation from target corpus) is high?

Or would you adopt a strategy where the actual corpus always hovers close to the target corpus during any month of the journey? This may not succeed all the time, but at least you will not fail badly. This is where goal-based investing makes the difference. Our focus shifts from returns and gains to one simple question: Are we on the right track at any point in the investment journey?

The problem is, investors tend to assume they can handle huge market crashes and years of poor equity returns without any practical investing experience – hence such notions of more equity upfront is born.

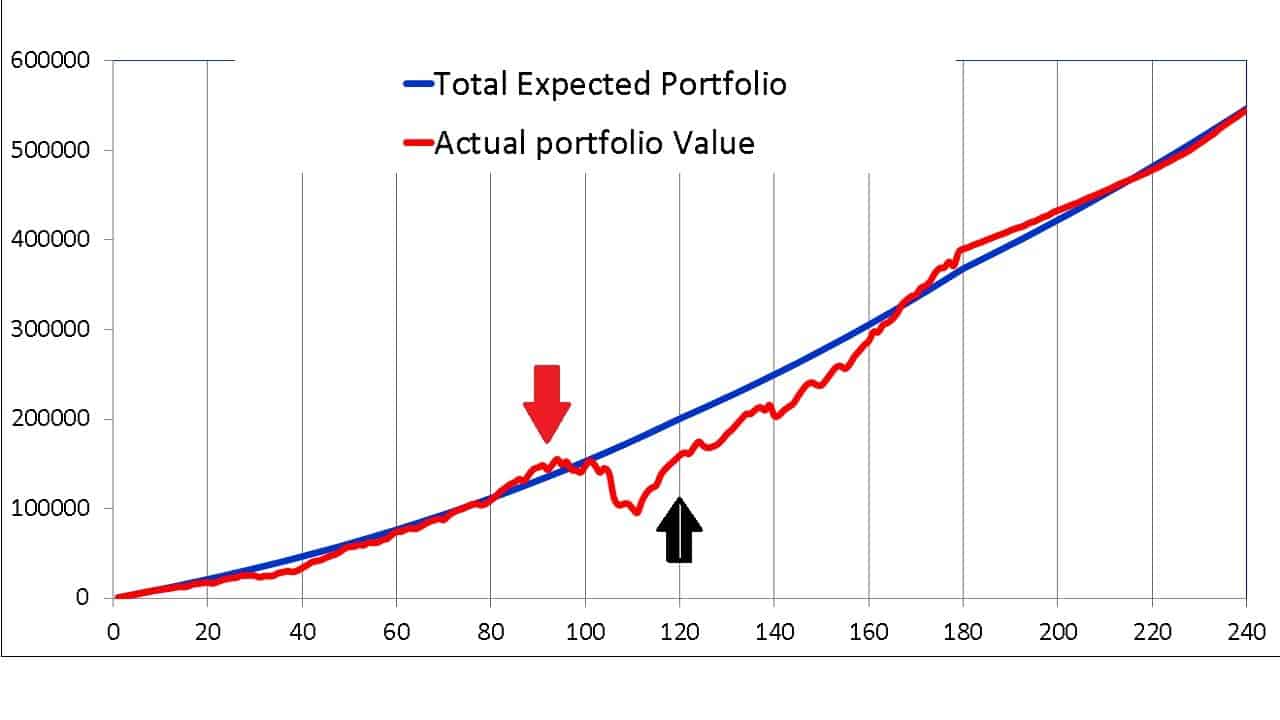

Take an example of a 20-year monthly return sequence below. The above four-pane result was obtained by iterating through 421 such sequences.

The hopeful investor sees that at the end of 20 years (x-axis is month number), the actual corpus is about equal to the target corpus for 100% equity in the first ten years + 60% equity for 5 years and zero for the last 5 years.

The cautious investor would know that the above is hindsight. If we sit on the red arrow, it is about 90 months since we started investing in 100% equity, and things look good. Yet after 120 months of 100% equity, the actual corpus is well below the target and takes another 4 years to recover!

How many investors can handle this? Of course, very few would know how to evaluate their portfolio this way and would either quit or plough through due to ignorance. Surely our money deserves better respect and planning than that!

The hopeful investor might criticise that we are looking at a cherry-picked bad result. The cautious investor would say: never cherry-pick high returns but always cherry-pick high risk! It is that high-risk scenario we need to prepare ourselves for.

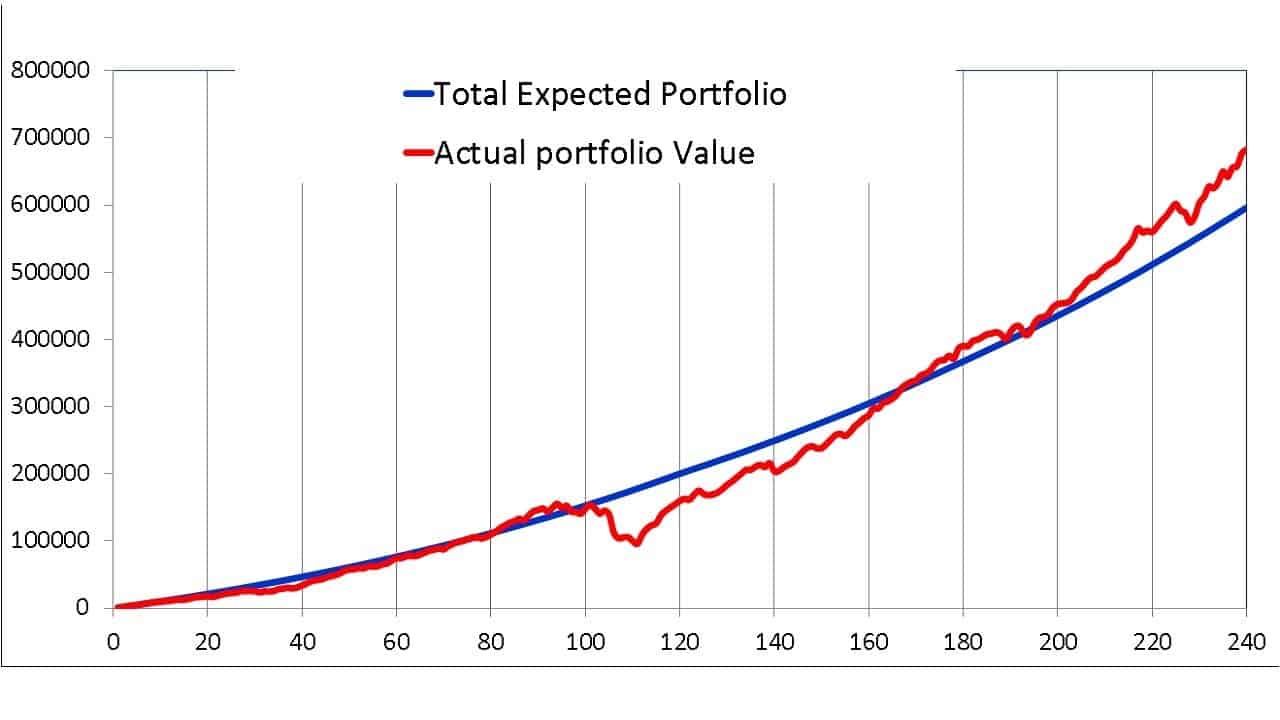

Take another asset allocation sequence for the same return sequence: 100% equity 10 years then 50% equity for ten years.

What do you see? Do you see risk in the journey, or do you see the reward at the end? The problem with hindsight bias is that it creeps up on us so silently that it is hard to detect.

In summary, a 100 equity allocation initially may work (or may not!), but it is pretty much guaranteed to be a rough ride for the investor – particularly those with theoretical knowledge bravado of what to do when they see a lion in the forest.

For an investor who appreciates that the goal of investing is not high returns but an adequate corpus for future needs, a healthy mix of equity and fixed income allocation from day one is the way to go. This will help you keep a calm head and learn more about systematically reducing risk in the portfolio. If you a new investor, you can consider watching this seminar: Basics of portfolio construction: A guide for beginners

Have a question? Subscribe to our newsletter and reply to any emails you get. I will not provide personal investment advice, but I will do my best to respond if you have a generic investing question. If it appeals to a wide audience, create an article/video about it.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

🔥You can also avail massive discounts on our courses and the freefincal investor circle! 🔥& join our community of 8000+ users!

Track your mutual funds and stock investments with this Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds, and ETF screeners, as well as momentum and low-volatility stock screeners.

You can follow our articles on Google News

We have over 1,000 videos on YouTube!

Join our WhatsApp Channel

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalised investment advice. We can write a detailed article without mentioning your name if you have a generic question.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

About The Author

Dr M. Pattabiraman (PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over 14 years of experience publishing news analysis, research and financial product development. Connect with him via Twitter(X), LinkedIn, or YouTube. Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.

Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! ⇐ More than 3,500 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Increase your income by getting people to pay for your skills! ⇐ More than 800 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner seeking more clients through online visibility, or a salaried individual looking for a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you. (watch 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our book for kids: “Chinchu Gets a Superpower!” is now available!

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting a side income via content writing. It is available at a 50% discount for Rs. 500 only!

Do you want to check if the market is overvalued or undervalued? Use our market valuation tool (it will work with any index!), or get the Tactical Buy/Sell timing tool!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy. Freefincal is a News Media organisation dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News. Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact Information: To get in touch, please use our contact form. (Sponsored posts or paid collaborations will not be entertained.)

Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner.

Our publications

You Can Be Rich Too with Goal-Based Investing

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.Your Ultimate Guide to Travel

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)