Mr Sharma (a pseudonym for perhaps your father, uncle, or neighbour) is a success story of the great Indian middle-class dream.

He grew up in an India of scarcity—ration cards, waiting years for a telephone connection, and job security being the ultimate prize. For 40 years, he worked tirelessly in a PSU or a corporate job. He walked to the bus stop to save the autorickshaw fare. He wore shirts until the collars frayed. He sacrificed vacations to pay for IIT coaching and his children’s grand weddings.

Today, at 68, Mr. Sharma is sitting on a paid-off house in a decent locality and a retirement corpus of over ₹3 Crores in FDs, PPF, and mutual funds.

He has won the game. He is financially free.

Yet, last night in the peak of May summer heat, Mr. Sharma woke up sweating because he switched off the AC after running it for exactly one hour. Why waste electricity? he murmured.

🔥Secure your future with our Robo-advisory tool trusted by over 3,000 investors and advisors. From effortless retirement planning to funding your children’s biggest dreams, turn your financial goals into reality. 🔥

Subscribe for money management solutions via email! (Link takes you to our email sign-up form) Join 32,000+ readers in our community.

👉 New Tool Alert! NaviPlan: A Privacy-Focused Multi-asset Tracker and Goal Planner 👈

This is the tragedy of the modern Indian retiree. They are asset-rich, cash-rich, but lifestyle-poor.

They are suffering from what financial psychologists call The Switch Failure (Inability to spend).

About the author: Ajay Pruthi is a fee-only SEBI-registered investment advisor. He can be contacted via his website plnr.in.

The Psychology of the Eternal Saver

For four decades, the switch in their brain was welded tight to the SAVE position. Every financial decision was filtered through the lens of accumulation. Saving wasn’t just a habit; it was a survival mechanism against an uncertain future in a developing economy.

Then, on the day of retirement, they are suddenly told to flip that switch to SPEND.

They physically cannot do it.

The neural pathways built over 40 years of frugality are too strong. To a lifelong saver, spending money—specifically, decumulating their hard-earned principal—registers in the brain almost like physical pain or moral failure.

They feel they are chopping down the tree they spent their whole life watering.

Symptoms of The Switch Failure in India

You see this manifested in countless Indian households where the parents have more than enough money, yet live in self-imposed austerity:

- The FD Interest Trap: They will only spend the interest earned from Fixed Deposits. Touching the principal amount feels like committing a sin. As inflation rises and interest rates fluctuate, their lifestyle shrinks, even though the principal remains untouched.

- The Medical Delay: They will have crores in the bank, but will delay a necessary knee replacement surgery or cataract operation for years because it costs too much right now.

- The Travel Paradox: At 70 years old, with bad backs, they still book Sleeper Class train tickets for overnight journeys instead of a comfortable 2AC or a flight, simply because the train gets us there too.

- The Inheritance Burden: A uniquely Indian pressure is the deep-seated belief that the entire corpus must be preserved for the children. They live like paupers so their 45-year-old, well-settled children can inherit a massive fortune later.

The Great Fear: What if I live too long?

The engine driving this inability to spend is a deep, primal fear of running out of money.

Indian retirees have seen inflation destroy the value of the Rupee over decades. They don’t trust that ₹3 Crores today will be enough 20 years from now when a hospital room might cost ₹50,000 a night.

So, they create a hyper-conservative buffer. They prepare for the absolute worst-case scenario (living to 105 with major medical needs), and in doing so, they completely miss out on the best-case scenario—enjoying the healthy years they have left.

The Final Destination: The Richest Corpse

The tragic outcome of The Switch Failure is a life unlived.

They sacrificed their 30s, 40s, and 50s for a someday of comfort. But when the day arrives, they are too psychologically damaged by years of scarcity to embrace it.

They become the richest people in the graveyard. They leave behind massive bank balances, perfectly preserved houses, and unspent lockers full of gold jewellery. Their children inherit wealth they often don’t urgently need, while the parents die with regrets of trips not taken, comforts not bought, and generosity not shared.

Flipping the Switch: How to enjoy the harvest

If you, or your parents, are stuck in this trap, logic won’t fix it. Emotional re-framing is needed.

- The Permission to Spend Fund

Create a separate bank account funded by a small portion of the corpus. The rule for this account is simple: This money must be wasted. It cannot be saved, invested, or given to kids. It must be spent on frivolous joy—a luxury hotel stay, a new car, a hobby. If it isn’t spent by the end of the year, it’s donated.

- The Bucket Strategy

Divide the wealth. Bucket A is untouchable survival money for medical needs and basic living until age 85/90. Bucket B is lifestyle money. Once Bucket A is secure, the brain relaxes, making it easier to spend from Bucket B without the panic of running out.

- Shift the Inheritance perspective

The greatest gift a parent can give adult children isn’t a massive inheritance when the children are already 50 years old. The greatest gift is being happy, healthy, and financially independent parents who enjoy their own lives. Your children want to see you spend your money on you.

The Bottom Line:

Money is stored energy. You spent your life accumulating this energy. If you don’t release it in the form of joy, comfort, and experiences while you are alive, that energy goes to waste.

You didn’t work for 40 years just to be the wealthiest patient in the hospital ward. Flip the switch. Buy the ticket. Turn on the AC. You earned it.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

🔥You can also avail massive discounts on our courses and the freefincal investor circle! 🔥& join our community of 8000+ users!

Track your mutual funds and stock investments with this Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds, and ETF screeners, as well as momentum and low-volatility stock screeners.

You can follow our articles on Google News

We have over 1,000 videos on YouTube!

Join our WhatsApp Channel

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalised investment advice. We can write a detailed article without mentioning your name if you have a generic question.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

About The Author

Dr M. Pattabiraman (PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over 14 years of experience publishing news analysis, research and financial product development. Connect with him via Twitter(X), LinkedIn, or YouTube. Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.

Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! ⇐ More than 3,500 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Increase your income by getting people to pay for your skills! ⇐ More than 800 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner seeking more clients through online visibility, or a salaried individual looking for a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you. (watch 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our book for kids: “Chinchu Gets a Superpower!” is now available!

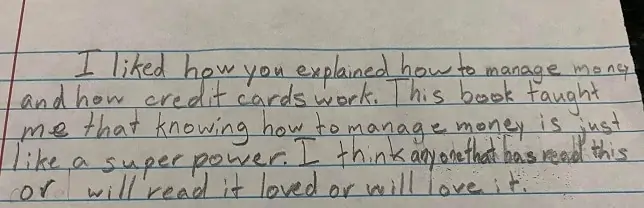

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting a side income via content writing. It is available at a 50% discount for Rs. 500 only!

Do you want to check if the market is overvalued or undervalued? Use our market valuation tool (it will work with any index!), or get the Tactical Buy/Sell timing tool!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy. Freefincal is a News Media organisation dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News. Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact Information: To get in touch, please use our contact form. (Sponsored posts or paid collaborations will not be entertained.)

Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner.

Our publications

You Can Be Rich Too with Goal-Based Investing

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.Your Ultimate Guide to Travel

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)