Last Updated on October 8, 2023 at 1:37 pm

Each week I try to answer generic reader questions on money management. Here is this weeks edition.

Hi Sir, I follow your blog regularly – you helped in a great deal choosing the right funds as per goals. Now, my question is – when is a good time for a retail investor to consider portfolio management scheme(PMS) and what are some of the good PMS providers in India? What should be my selection criteria in selecting the correct PMS? Thank you.

Thank you. Mutual funds are way more convenient and tax efficient (stock buy and sells would results in short term and long term capital gains) than a PMS for everyone – retail or high net worth investor. So I would suggest that you do not consider a PMS. Keep it simple.

“If you must go by stars, choose a 3-star fund that has consistently beat the benchmark consistently over 3Y and more.” Can you please elaborate this? What benchmark the fund should be compared against? How can I know if it has beaten the benchmark consistently? – Sachin.

I keep saying this about 3-star funds just to highlight the fact a 3-star fund investor is likely to be calmer than a 5-star fund investor. If you were to track star rating history, you will notice (VR pointed this out) that very few funds stay in 4-,5-star range all their life.

Most 5-star funds are a flash in the pan. So the outstanding performance is typically temporary. If I choose a fund by its stars, I am likely to be disappointed if it falls in rating. Therefore, I would prefer not to look at stars at all.

🔥Secure your future with our Robo-advisory tool trusted by over 3,000 investors and advisors. From effortless retirement planning to funding your children’s biggest dreams, turn your financial goals into reality. 🔥

Subscribe for money management solutions via email! (Link takes you to our email sign-up form) Join 32,000+ readers in our community.

👉 New Tool Alert! NaviPlan: A Privacy-Focused Multi-asset Tracker and Goal Planner 👈

What benchmark to use? The total returns index (TRI) of the benchmark that the fund uses. The TRI assumes dividends are reinvested and this is harder to beat than just the price index.

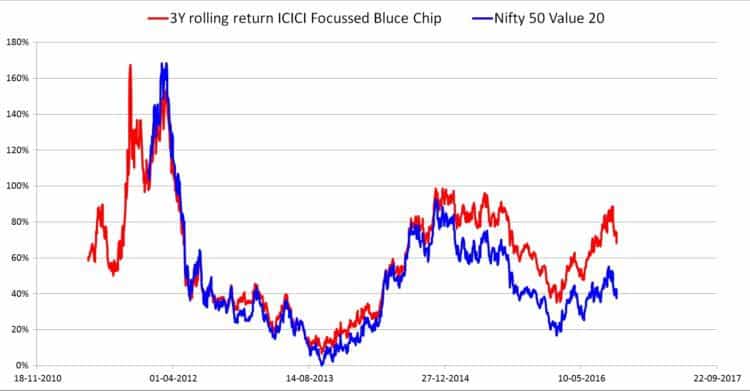

How to evaluate performance consistency? Use a rolling returns calculator. Here the duration over which the return is computed is “rolled over” to the next business day.

For example, suppose we wish to analyse the fund from Jan 2006, we calculate the return over 3 years (say) between

Jan 1st 2006 to Dec 31st 2008 and then between

Jan 2nd 2006 to Jan 1st 2009 and then between

Jan 3rd 2006 to Jan 2nd 2009 and so on. That is over every possible 5 year period. Then we repeat this for the benchmark and get a graph like this:

Notice that it immediately tells you that the fund has been consistent in beating the benchmark.

Whether it is a 1-star fund or 5-star fund, as long as it is consistent this way, I will be happy to invest in it.

Readers have two options:

Use this for individual funds and their specific benchmarks: Mutual Fund SIP and Lump Sum Rolling Returns Calculators

Or, use the monthly outperformance screener: January 2017: Equity Mutual Fund Outperformance Screener

What is your opinion on the FundsIndia Super Savings Account which invests your idle cash in Reliance Money Manager liquid fund? – Mahesh

As long as the short term, medium term and long term financial goals are accounted for, the rest of the available must be idle! It can be in a savings bank account or a liquid fund. It does not matter where. If you wish to use the above-mentioned reliance fund, get an account with them and invest directly.

Post my financial audit on Jan 2017, I find that my retirement portfolio has reached the ratio of 50:50 w.r.t equity:debt. My equity return assumption is 12% and Debt 8% and hence my portfolio return expectation is 10%. Retirement is 20+ years away. Though I can take this to 60:40, but it will not bring a significant increase in return expectation. (With 60:40 and 12% vs 8%, return expectation is only 10.40% as opposed to 10% flat for 50:50). I want to stick to 50:50. Till now, I invested only in equity for which I am now at 50:50. Therefore, now on, I would require to invest in Debt MF as well, in addition to EPF, for keeping equity debt ratio at 50:50 levels. For retirement purposes and long term debt investment, what can be the right category of Debt mutual funds ? Till now, the UST category has returned same as other Debt fund categories over a long period of time. But is there any merit to invest in Dynamic Bond or Income funds when the goal is more than 15 years away. How rewarding or punishing can be if someone embraces volatility in debt funds ? Or should I stick to plain vanilla liquid or UST ? – Anish.

The answer is quite contextual. For you, I would say, if it will not clutter your portfolio, you can have some corporate bond or income fund exposure. However, is it really necessary when you can add more into EPF? You still get solid returns there, with same liquidity.

Should the investment in equity arbitrage fund be considered as equity investment? – Abhay

We should consider it as a debt instrument because of its risk profile. The taxman treats it as equity wrt taxation.

I am investor in mutual funds. I started late my asset allocation is equity 30% and debt 70%. I want to increase this to 50-50. Currently investing via SIP 20000 pm for 3 years in each of mirae asset emerging bluechip, franklin india smaller companies and franklin india prima fund. All direct. I will not require this money for 10 years as this is for my retirement. I will retire after 3 years so can invest in this period only. I have income from other sources to take care of retirement expenses initially. But I have option to invest additional amounts in these schemes as I have extra money now in my savings account (INR 1,000,000). What should be criteria for additional investments? Should I see PE of each of these funds or is there some better way? Basically my question is, if someone has additional amount for investing then what should be the criteria? Sandeep Gupta

The PE of a mutual fund has not much relevance to the investor. At best it can provide a subjective insight into the fund managers strategy. You can continue to invest systematically. I would suggest a rethink into your equity allocation. You cannot make up for lost time by having 50% equity for 7 years into retirement. That is quite dangerous.

Suggest that you plan your retirement expenses with this one of these tools:

Retirement Calculator for the Middle-aged Employee

Inflation-protected Income Simulator

I own a small business. My cash flow is erratic so i can’t commit to a fixed SIP schedule. For last few months, I am investing in ICICI Pru, Axis Long Term and HDFC Mid cap every month randomly. Do mutual funds have P/E ratios? Before investing, should i look at current P/E value for that fund? If Yes, where can i find current/ most recent P/E value for a mutual fund .. and what is the good enough p/e range to invest. – Santosh

Yes, mutual funds have PE ratios, but as mentioned above, they are of little use. You can check Value Research or Morning Star for the PE. Most mutual funds change their portfolios frequently. So, there is no value in looking at a funds portfolio PE. Simply invest when you can. No big deal.

There are 7 more questions to discuss. Will do that tomorrow.

Ask Questions with this form

And I will respond to them next week. I welcome tough questions. Please do not ask for investment advise.

Error: Contact form not found.

Pune Investor Workshop Feb 26th 2017

The second Pune workshop will be held on Feb 26th 2017. You can register for this via this link

You Can Be Rich Too With Goal-Based Investing

Your first investment should be buying this book

The (nine online) calculators are really awesome and will give you all possible insights

Thank you, readers, for your generous support and patronage.

Amazon Hardcover Rs. 266. 33% OFF

Kindle at Amazon.in (Rs. 244.30)

Google Play Store (Rs. 244.30)

Now just Rs. 265 offer valid only today at Infibeam

If you use a mobikwik wallet, and purchase via infibeam, you can get up to 100% cashback!!

- Ask the right questions about money

- get simple solutions

- Define your goals clearly with worksheets

- Calculate the correct asset allocation for each goal.

- Find out how much insurance cover you need, and how much you need to invest with nine online calculator modules

- Learn to choose mutual funds qualitatively and quantitatively.

More information is available here: A Beginner’s Guide To Make Your Money Dreams Come True!

What Readers Say

Also Available At

Bookadda Rs. 371. Flipkart Rs. 359

Amazon.com ($ 3.70 or Rs. 267)

Google Play Store (Rs. 244.30)

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

🔥You can also avail massive discounts on our courses and the freefincal investor circle! 🔥& join our community of 8000+ users!

Track your mutual funds and stock investments with this Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds, and ETF screeners, as well as momentum and low-volatility stock screeners.

You can follow our articles on Google News

We have over 1,000 videos on YouTube!

Join our WhatsApp Channel

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalised investment advice. We can write a detailed article without mentioning your name if you have a generic question.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

About The Author

Dr M. Pattabiraman (PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over 14 years of experience publishing news analysis, research and financial product development. Connect with him via Twitter(X), LinkedIn, or YouTube. Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.

Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! ⇐ More than 3,500 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Increase your income by getting people to pay for your skills! ⇐ More than 800 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner seeking more clients through online visibility, or a salaried individual looking for a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you. (watch 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our book for kids: “Chinchu Gets a Superpower!” is now available!

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting a side income via content writing. It is available at a 50% discount for Rs. 500 only!

Do you want to check if the market is overvalued or undervalued? Use our market valuation tool (it will work with any index!), or get the Tactical Buy/Sell timing tool!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy. Freefincal is a News Media organisation dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News. Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact Information: To get in touch, please use our contact form. (Sponsored posts or paid collaborations will not be entertained.)

Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner.

Our publications

You Can Be Rich Too with Goal-Based Investing

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.Your Ultimate Guide to Travel

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)