Last Updated on December 19, 2021 at 7:19 pm

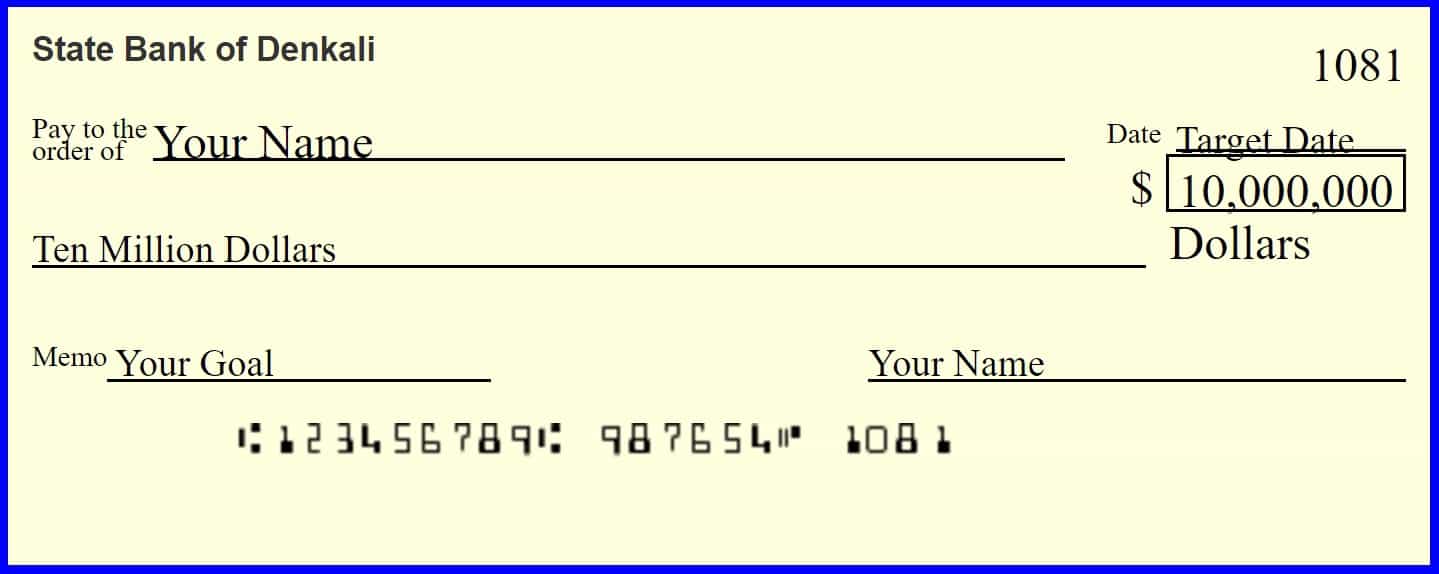

Now, why stop at one crore? Make that a Ten Crore Cheque. If you are wondering whether you have landed at the wrong site or if something is wrong with me, not to worry. I am not any more mentally disabled than I was yesterday, and you are at freefincal. Allow me to explain. How does one get rich? What is the first step towards financial independence? Crude as it may seem, the first step to be rich is think you will be rich. The first step to financial independence is a clear purpose. Not a higher a salary as many mistakenly believe.

Sure a higher salary will help hasten the process, but it is the purpose that counts -the desire to change the way and your family have been handling money. Here are two fascinating anecdotes.

Jim Carrey

Jim Carrey is a versatile actor, best known for his comic roles. He hails from an extremely poor background. His family lived off a van in Canada, and at age 16, he quit school to become a full-time custodian (a Janitor). Prior to that, he had an 8-hour shift after school helping his father on the same job. (source, plus many others online)

In the early 90s, he wrote himself a cheque for 10 million dollars for acting services rendered and dated it Thanksgiving 1995 ( 2nd Monday of October in Canada or 4th Thursday of Nov in USA) 1995 and put it in his wallet. Just before said date, he was paid 10 million dollars for Dumb & Dumber. As Oprah Winfrey so rightly puts it in this interview (youtube) ,

🔥Secure your future with our Robo-advisory tool trusted by over 3,000 investors and advisors. From effortless retirement planning to funding your children’s biggest dreams, turn your financial goals into reality. 🔥

Subscribe for money management solutions via email! (Link takes you to our email sign-up form) Join 32,000+ readers in our community.

👉 New Tool Alert! NaviPlan: A Privacy-Focused Multi-asset Tracker and Goal Planner 👈

Jim Carrey visualised himself as rich and visualisation works if you work hard

To which Jim replies,

Yes, you cannot visualise and go eat a sandwich!

When his father passed, Carrey placed the cheque in his father’s casket because it was “our dream, together”.

What’s that? Do I hear you say, this is more an exception than an example? That JIm Carrey is super-talented and he would have made it big anyway? Hmm.. I don’t agree, but all right. Here is another.

Mr. Lastbencher

This is about my college mate who was a last bencher both in location and behaviour. He did not appear one bit interested in doing what he was supposed to do – study physics. Cut to 22 years later, a mutual friend tells me, that Mr. Lastbencher is retired!

So I befriend him on Facebook and messaged for details. Months pass before he sees the message. He eventually told me that “it is no big deal”. He wanted to retire by 40 and did by 39. He left a top job with a sweet severance deal and for the last four years has spent half his time on the road with his Royal Enfield. For the rest of the time, he is at home and sometimes drives a cab to pass the time!

I asked him how he did it and he says, (a) closed out loans, (b) reduced his needs to achieve his goal, and (c) invested right.

Now, what do you say to that?! He would have easily been a contender for the “least likely to succeed” award based on the evidence available to us 22 years ago. Now, look at him! Please do not look at his position or the severance deal. Focus on his desire to live his dreams by a certain age. Focus on how fast he must have risen up the company ranks and the hard work associated with it. Focus on his planning, his cutting needs short.

Most importantly, focus on the fact that he exhibited no special talents. He was only passionately driven (à la Einstein). Most education systems have no way to judge this. Academic performance can neither reflect intelligence or passion – at least that is what I tell my students each semester. As long as a student get her act together at some point in life, she should be fine. Mr. Lastbencher is a fine example of this.

He shall be unnamed for this post because I have not sought his permission (it may take months to get a response) and he may not agree! It is better this way and his name and other details are of little relevance to the present context.

What is common between these two tales?

Tamil actor Vijay Antony sums it up quite well. When asked “how he did it”, he said:

I knew where I was today and I knew where I wanted to be tomorrow. So I did what was necessary to go there.

That is it. Pure and simple – a clear purpose followed up with the necessary effort.

Nothing to do with how much they earned. Sure the quantum of money earned will decide how sooner or later financial independence is achieved. But it is not a race. There is no special award for getting there earlier. And not all can get there at the same time.

This is about the intent and the journey.

So let us go ahead and visualise ourselves as rich. Write that cheque for Ten Crores.

Let us ignore trivialities (discounts, reward points, cashbacks, charges, fees, 0.5% drop in interest rates etc) and focus on the big picture (start early, invest right and invest big). The first step in getting rich is to believe without a shred of doubt that we will be. It is just a matter of time and effort.

The first step in getting rich is to believe without a shred of doubt that we will be. It is just a matter of effort and time (in that order).

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email!(Link takes you to our email sign-up form)

Use our Robo-advisory Tool to create a complete financial plan! More than 3,000 investors and advisors use this! Use the discount code robo25 for 20% off. Plan your retirement (early, normal, before, and after), as well as non-recurring financial goals (such as child education) and recurring financial goals (such as holidays and appliance purchases). The tool would help anyone aged 18 to 80 plan for their retirement, as well as for six non-recurring and four recurring financial goals, with a detailed cash flow summary.

🔥You can also avail massive discounts on our courses and the freefincal investor circle! 🔥 & join our community of 8000+ users!

Track your mutual funds and stock investments with our Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds, ETF screeners, as well as momentum and low-volatility stock screeners.

You can follow our articles on Google News

We have over 1,000 videos on YouTube!

Podcast: Let's Get RICH With PATTU! Every single Indian CAN grow their wealth!

You can watch podcast episodes on the OfSpin Media Friends YouTube Channel

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalised investment advice. We can write a detailed article without mentioning your name if you have a generic question.

About The Author

Dr M. Pattabiraman (PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over 14 years of experience publishing news analysis, research and financial product development.

Connect with him via Twitter(X) LinkedIn YouTube

Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! More than 3,500 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Increase your income by getting people to pay for your skills! More than 800 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner seeking more clients through online visibility, or a salaried individual looking for a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you. (Watch the 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our book for kids: “Chinchu Gets a Superpower!” is now available!

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.

Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting a side income via content writing. It is available at a 50% discount for Rs. 500 only!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy

Freefincal is a News Media organisation dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News.</p river> Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact Information: To get in touch, please use our contact form. (Sponsored posts or paid collaborations will not be entertained.)Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner

Our publications

You Can Be Rich Too with Goal-Based Investing

Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

Your Ultimate Guide to Travel