Last Updated on October 8, 2023 at 1:37 pm

Each week, I try and answer generic questions from readers. Here is part one of this week’s edition. If you have a question, please use the form below. Please note that I will not provide specific investment advice and/or product suggestions.

Pattu Sir, can any MF CAGR could be 24%? How can i get returns about real estate from some website or so like for equity and MF. I want to check YoY returns of the Real Estate especially in Bangalore? Krishnapratap

Anything is possible, that does not mean I should expect such returns! Real estate is an unorganised business and a commonly accepted fair market value is not possible like equity. The recent push for digital transactions should change this. The only way to know yoy returns is for you to talk to brokers and determine price yourself.

Pattu Sir, I am 39 now and started SIP in MF 1 year back. I am earning 10 lacs p.a. I have 3 years daughter and from this june she will go to school. The annual fees is 1.2 lacs. Also, i want to buy a car and budget home in Bangalore and do not have money for 20% down payment as well and when i see the EMI amount for 20 years tenure as well as interest on it for 30 to 40 lacs apartment then it looks too much and don’t know when can i afford for a house. I am the only person earning and need some suggestion from you on it as i have to fulfill many goals like daughter’s education, marriage, retirement, buying house, etc. Krishnapratap

You are not alone! Practically everyone, including myself, has this problem. There is not much of a solution. Get priorities right. For me, retirement comes first and then child’s education and then others. I will invest what I can and be patient if there are decent growth prospects for my salary. Else, I will have to either find a way to earn more or dream less!

A couple of posts that may cheer you up:

🔥Secure your future with our Robo-advisory tool trusted by over 3,000 investors and advisors. From effortless retirement planning to funding your children’s biggest dreams, turn your financial goals into reality. 🔥

Subscribe for money management solutions via email! (Link takes you to our email sign-up form) Join 32,000+ readers in our community.

👉 New Tool Alert! NaviPlan: A Privacy-Focused Multi-asset Tracker and Goal Planner 👈

Do not be scared by what you need to accumulate for retirement!

Why is the retirement corpus I need so large?!

Hi Sir, Do we need to consider Exit Load(1% for redemption within 2 years) while choosing Mutual Fund ? Abbas

For long term goals, it should not matter much. For systematic investing, it should not matter much as we have little control. While investing a lump sum in a debt fund for a short while, you may want to keep an eye on exit load. However, that is not as important as where you are investing in.

Hello Mr. Pattu, I’ve been using your Automated MF planner to track my goals. Some of my long term goals have turned -ve (from a monthly investment perspective) what does this mean & how to interpret it? Thanks, Anand.

This is the tracker being referred to: Features of the freefincal mutual fund and financial goal tracker. I use only this tool to track and review my portfolio and have set it up such that I an audit my finances automatically. I will post a video on how to use this tracker soon.

Reviewing a long-term goal in terms of monthly investment required is a pretty smart idea. IF the inputs are right/reasonable and if the monthly investment required keeps decreasing, this means the corpus is growing at a healthy pace. If it becomes negative, it means you do not have to invest anymore! However, please check and double-check your requirements and inputs before concluding that!

Read more: The 2016 Personal Finance Audit: Returns do not matter!

Hi Pattu Sir Subra told in his blog don’t invest in opportunities fund. let me know why one should not consider investing in opportunities mutual fund? Ramesh

I used Google to understand the context, and I think by opportunities funds he is referring to equity funds with a specific flavour – sector funds. That is a concentrated portfolio. This is common sense 101 for most investors: be diversified at all times.

Why worry about Risk?

The so-called “risky” mid cap funds managed to beat bluechip returns over 5 and 10 yr periods. Does it mean the risk of mid-cap funds get neutralised over long periods and one can solely invest in these funds? And why is risk important to a portfolio as long as decent returns are generated? – Ranjan.

Imagine a race from town A to town B. You can either use the highway or cut across the country for the journey. If the aim is to finish first and you know the cross country route is shorter, would you use the same car that you drive in cities or would you choose an all-terrain vehicle with better suspension and tires?

The reward (finishing faster/first) requires managing risk (choosing the right equipment). They cannot be separated.

The problem is not with the choice of the road (highway or cross-country; large-cap or mid-cap) but with risk management (or lack thereof: using a city car on rough terrain or holding mid-caps with the hope that they would return better).

I am afraid looking at 5Y or 10Y returns alone is hindsight bias based on a couple of data points. The assumption typically involved when someone says, “hold more of mid-cap and small-caps” is that the no matter how volatile the markets are “today” and in the “near future”, it will eventually go up and we can reap benefits.

If this is the intended strategy, I am afraid it is silly. Take any sideways market and you will find that large-caps outperform the mid and small caps.

If my retirement is 25 years away, I can handle a sideways market of say 5 years today. Can I endure this 10 Y later? or 15Y later? It would be foolhardy to do so in the hope the market will eventually go up. And with time, my equity exposure will also need to go down.

This is where the idea of the sequence of returns matter. This is the annual returns of Franklin India Prima Fund from Value Research.

Now please project such returns in future. There would be some years of spectacular returns and some years where a large-cap or mid-cap fund would fail to beat a fixed deposit. The gains made in 5-6Y can be lost in a single year. The opposite is also true.

I have no issues with investing in 100% of mid-cap and small-cap funds. My own portfolio should have anywhere between 40-50% exposure to such funds.

My problem is with assuming 100% mid-caps will do better than 50% mid-caps. This may be possible for only some sequence of returns. The key point to remember is that we do not know what sequence we are going to get in future.

Which is a why a diversified equity portfolio would lower the range over which returns can fluctuate. Sure, final returns maybe lower but at least it will keep an investor calm(er). I would prefer a calmer but potentially less fruitful path any day: choose a reasonably strong city car on a highway.

Risk and reward cannot be viewed separately. When I look at ten-year returns, I do not look at the journey. The ups and downs are all washed away. Sure, someone may have driven a city car cross country and succeeded. Does that mean you will too? Hope and bravado are not strategies.

Most people I know claim that they can handle volatility without any evidence of experience or at least a plan for of doing so. Excuse me for not taking them seriously.

Handling here refers to risk management. All equity investing requires active management to de-risk the investment portfolio. A 100% large cap folio would require lesser management than a 50% large cap folio, which in turn would require lesser risk management than a 100% mid/small cap folio.

So if you want to avoid large caps, have a strong risk management strategy in place and then hope for the best. Please do not assume based on “past performance” that one type of investment choice will triumph over others.

There is a difference between instrument returns and investor returns.

Not only should we choose the right car, we should also have a plan in case it breaks down.

Hello sir, please suggest me a mutual fund for short term period, which can earn me more than banks FD. All I need is a risk free or very very less risk fund.

1: I do not recommend fund names and 2: I do not know what your idea of short-term is. Assuming it is less than 5Y, I would recommend the use of a liquid fund or ultra short term fund with no guarantee of beating an FD. Over that time period, there is no need to beat the returns of an FD!

Hi Pattu, About Credit Cards, I don’t have one and find that I am the only one in my office(also among my circle) going on in life without a credit card. Is there a need for a credit card? in a salaried person’s life. Whether the return in terms of points / cashback @1% – 3% justify the use of a Credit card. I see that credit cards have some perks like Lounge Access in International Airports etc. Still I am in a dilemma, as I have plan of International Tour this year. Should I take credit card? Pl help. Raj

If you are going abroad, you would need a valid credit card. I don’t have a credit card too and don’t think much about cashback and rewards. My wife has had a card for 14Y now and occasionally we do find some use for it. Never claimed any reward till now.

A credit card has an important use – it offers your short-term credit which has to be paid back in full before the due date. The reward points are just perks that one need not worry about. There are situations where payment can be made only via a credit card and abroad it is better to carry minimal cash.

1) How can somebody/blood relatives send money abroad from India? 2) Can you transfer money from your NRE/NRO account to your blood relatives’ account? 3) What is the procedure to repatriate money from NRE accounts?4 ) Can you transfer money from FCNR to NRE/NRO/ savings accounts of blood relatives? Thanks a ton for all the amazing blogs you write. Regards, Sachin

Sachin, this is not my area of expertise and therefore cannot comment on this. However, I see that Google provides detailed articles for each of your questions. You should be able to make better sense out of that than me!

I am a central government employee and covered under NPS. My contribution to NPS for the current year is Rs75000. I repaid home loan principal of Rs 92000 and paid insurance premium of Rs 25520. May I claim the money over and above Rs 150000 under 80 CCD 1b Thank you. Narayanan

Yes, you can claim 50K from your mandatory employee contribution under 80CC1(b) and use the rest + other avenues for the 80C benefit.

I shall cover the remaining questions tomorrow.

Ask Questions with this form

And I will respond to them next week. I welcome tough questions. Please do not ask for investment advice. Before asking, please search the site if the issue has already been discussed. Thank you.

Error: Contact form not found.

Pune Investor Workshop Feb 26th, 2017

The second Pune workshop will be held on Feb 26th, 2017. You can register for this via this link

You Can Be Rich Too With Goal-Based Investing

The best book ever on Financial Freedom Planning. Go get it now!

Your first investment should be buying this book

The (nine online) calculators are really awesome and will give you all possible insights

Thank you, readers, for your generous support and patronage.

Amazon Hardcover Rs. 338 15% OFF

Kindle at Amazon.in (Rs. 244.30)

Google Play Store (Rs. 244.30)

Infibeam Now just Rs. 307 use love10 to get additional 10% OFF.

If you use a mobikwik wallet, and purchase via infibeam, you can get up to 100% cashback!!

- Ask the right questions about money

- get simple solutions

- Define your goals clearly with worksheets

- Calculate the correct asset allocation for each goal.

- Find out how much insurance cover you need, and how much you need to invest with nine online calculator modules

- Learn to choose mutual funds qualitatively and quantitatively.

More information is available here: A Beginner’s Guide To Make Your Money Dreams Come True!

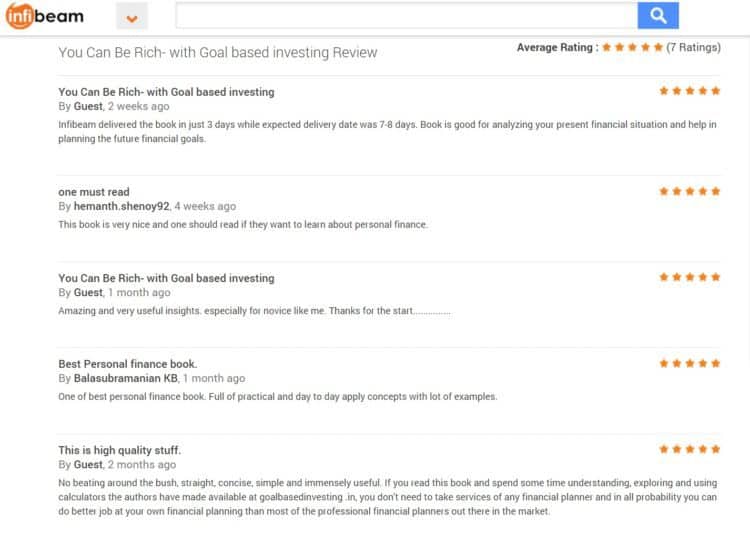

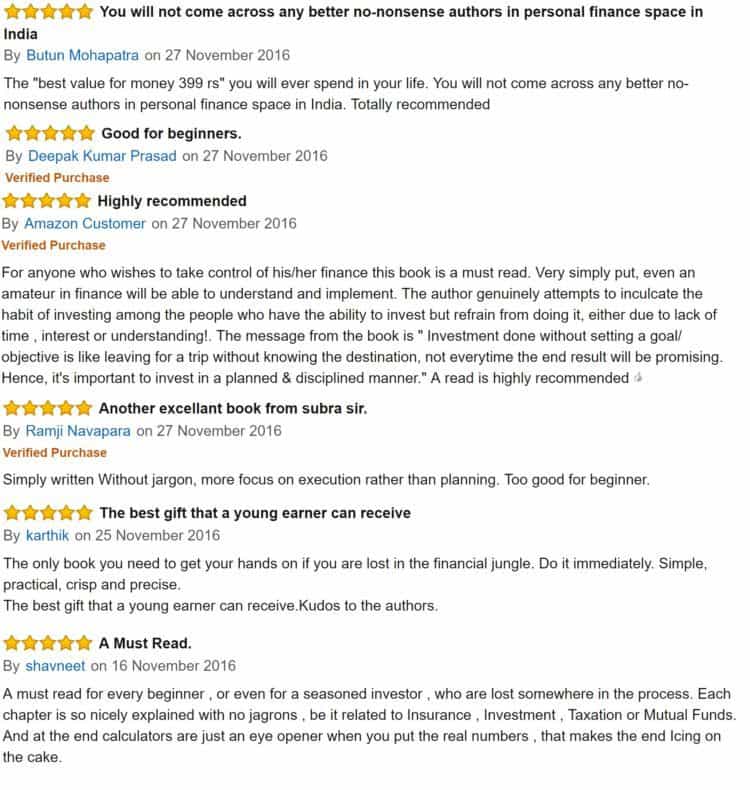

What Readers Say

Also Available At

Bookadda Rs. 371. Flipkart Rs. 359

Amazon.com ($ 3.70 or Rs. 267)

Google Play Store (Rs. 244.30)

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

🔥You can also avail massive discounts on our courses and the freefincal investor circle! 🔥& join our community of 8000+ users!

Track your mutual funds and stock investments with this Google Sheet!

We also publish monthly equity mutual funds, debt and hybrid mutual funds, index funds, and ETF screeners, as well as momentum and low-volatility stock screeners.

You can follow our articles on Google News

We have over 1,000 videos on YouTube!

Join our WhatsApp Channel

- Do you have a comment about the above article? Reach out to us on Twitter: @freefincal or @pattufreefincal

- Have a question? Subscribe to our newsletter using the form below.

- Hit 'reply' to any email from us! We do not offer personalised investment advice. We can write a detailed article without mentioning your name if you have a generic question.

Join 32,000+ readers and get free money management solutions delivered to your inbox! Subscribe to get posts via email! (Link takes you to our email sign-up form)

About The Author

Dr M. Pattabiraman (PhD) is the founder, managing editor and primary author of freefincal. He is an associate professor at the Indian Institute of Technology, Madras. He has over 14 years of experience publishing news analysis, research and financial product development. Connect with him via Twitter(X), LinkedIn, or YouTube. Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.

Pattabiraman has co-authored three print books: (1) You can be rich too with goal-based investing (CNBC TV18) for DIY investors. (2) Gamechanger for young earners. (3) Chinchu Gets a Superpower! for kids. He has also written seven other free e-books on various money management topics. He is a patron and co-founder of “Fee-only India,” an organisation promoting unbiased, commission-free, AUM-independent investment advice.Our flagship course! Learn to manage your portfolio like a pro to achieve your goals regardless of market conditions! ⇐ More than 3,500 investors and advisors are part of our exclusive community! Get clarity on how to plan for your goals and achieve the necessary corpus no matter the market condition!! Watch the first lecture for free! One-time payment! No recurring fees! Life-long access to videos! Reduce fear, uncertainty and doubt while investing! Learn how to plan for your goals before and after retirement with confidence.

Increase your income by getting people to pay for your skills! ⇐ More than 800 salaried employees, entrepreneurs and financial advisors are part of our exclusive community! Learn how to get people to pay for your skills! Whether you are a professional or small business owner seeking more clients through online visibility, or a salaried individual looking for a side income or passive income, we will show you how to achieve this by showcasing your skills and building a community that trusts and pays you. (watch 1st lecture for free). One-time payment! No recurring fees! Life-long access to videos!

Our book for kids: “Chinchu Gets a Superpower!” is now available!

Must-read book even for adults! This is something that every parent should teach their kids right from their young age. The importance of money management and decision making based on their wants and needs. Very nicely written in simple terms. - Arun.Buy the book: Chinchu gets a superpower for your child!

How to profit from content writing: Our new ebook is for those interested in getting a side income via content writing. It is available at a 50% discount for Rs. 500 only!

Do you want to check if the market is overvalued or undervalued? Use our market valuation tool (it will work with any index!), or get the Tactical Buy/Sell timing tool!

We publish monthly mutual fund screeners and momentum, low-volatility stock screeners.

About freefincal & its content policy. Freefincal is a News Media organisation dedicated to providing original analysis, reports, reviews and insights on mutual funds, stocks, investing, retirement and personal finance developments. We do so without conflict of interest and bias. Follow us on Google News. Freefincal serves more than three million readers a year (5 million page views) with articles based only on factual information and detailed analysis by its authors. All statements made will be verified with credible and knowledgeable sources before publication. Freefincal does not publish paid articles, promotions, PR, satire or opinions without data. All opinions will be inferences backed by verifiable, reproducible evidence/data. Contact Information: To get in touch, please use our contact form. (Sponsored posts or paid collaborations will not be entertained.)

Connect with us on social media

- Twitter @freefincal

- Subscribe to our YouTube Videos

- Posts feed via Feedburner.

Our publications

You Can Be Rich Too with Goal-Based Investing

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.

Published by CNBC TV18, this book is designed to help you ask the right questions and find the correct answers. Additionally, it comes with nine online calculators, allowing you to create custom solutions tailored to your lifestyle. Get it now.Gamechanger: Forget Startups, Join Corporate & Still Live the Rich Life You Want

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.

This book is designed for young earners to get their basics right from the start! It will also help you travel to exotic places at a low cost! Get it or gift it to a young earner.Your Ultimate Guide to Travel

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)

This is an in-depth exploration of vacation planning, including finding affordable flights, budget accommodations, and practical travel tips. It also examines the benefits of travelling slowly, both financially and psychologically, with links to relevant web pages and guidance at every step. Get the PDF for Rs 300 (instant download)